Do I need to pay tax if my income goes even one rupee over Rs 12 lakh?

Here are those questions that will be frequently asked for the rest of the year on income tax

By Adhil Shetty

As the ink dries on the Union Budget announcements, here are 7 questions that will be frequently asked for the rest of the year. While the answers may be straightforward for tax experts, laypersons may have a hard time understanding the new rules. So let’s address them.

How is Rs 12 lakh tax-free if there is a 5% and 10% tax respectively on incomes between Rs 4 and Rs 8 lakh and Rs 8 and Rs 12 lakh?

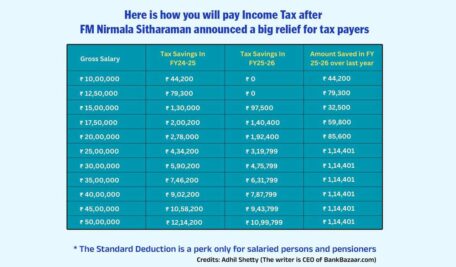

Forget the slabs for a second. Let’s understand the 87A rebate first. This rebate is like a 100% discount coupon on your food bill — but only up to a limit. That limit was Rs 20,000 last year. So, you did have a tax liability, but the government said, “No thanks, you can keep that money.” This made Rs 7 lakh tax-free. This year, that limit will rise to Rs 60,000. That will make income up to Rs 12 lakh tax-free. But if you’re over-limit, you will not get the 87A rebate.

But isn’t income up to Rs 12.75 lakh tax-free with Standard Deduction?

Yes, it is. You get a Standard Deduction of Rs 75,000 — but only if you’re salaried or a pensioner choosing the new tax regime. You have a few deductions in the new regime. With them, your taxable income (income after deductions and exemptions) of Rs 12 lakh or less become tax-free.

So if my taxable income goes even one rupee over Rs 12 lakh, do I need to pay Rs 62,400 as tax? That seems unfair.

Nope, you don’t! There’s something called marginal relief. It comes to your rescue. It ensures that your tax over the tax-free limit isn’t higher than the limit by which you went over.

Example: if your taxable income is Rs 12 lakh and Rs 100, your tax will be only Rs 100 + Rs 4 rupees for cess = Rs 104.

What if my income isn’t from salary or pension? Do I still get Rs 12 lakh tax-free?

Not quite. Think of the Rs 12 lakh tax-free benefit as coming from a two-part combo: the 87A rebate and the Standard Deduction of Rs 75,000. The catch? The Standard Deduction is a perk only for salaried folks and pensioners. If you’re earning through business, freelancing, or any non-salary route, you won’t enjoy that extra deduction. However, if your taxable income (excluding incomes like capital gains) stays within Rs 12 lakh, you can still benefit from the 87A rebate.

What about capital gains like profits from mutual funds and stocks?

Capital gains are a whole different ball game. They’re taxed separately at their own special rates, even if your salary qualifies for the tax-free benefit. In other words, even if your salary or other regular income is within the Rs 12 lakh limit, any profit you make from selling stocks or property (ie, capital gains) will be taxed on its own. So, capital gains don’t count toward that Rs 12 lakh magic number. They come with their own tax bill.

Do the new tax slabs apply right away?

The new tax slabs were announced in the Union Budget on February 1, 2025. The new rules become applicable from April 1, 2025, when the new financial year starts. Until then, you’ll pay the old rates announced last year.

What about the old regime? Should I stop using it?

About 72% of taxpayers have opted for the new regime, and with the new rules, 85-90% may have zero tax liability, making it the likely choice for most. However, individuals should compare both regimes. If your taxable income is Rs 5 lakh or less, both regimes offer zero tax liability. The new regime is now the default, but the old regime may still benefit those leveraging deductions like insurance, PF, home loans, rent, tuition fees, or capital loss carry-forwards.

(The writer is CEO of BankBazaar.com)

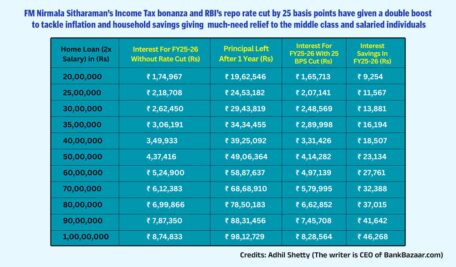

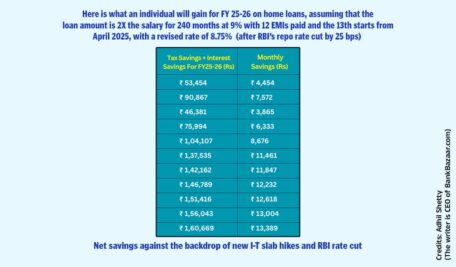

- Loan assumed as 2X salary for 240 months at 9% with 12 EMIs paid, and the 13th EMI starts from April 2025 with a revised rate of 8.75%

- A salaried person with a gross income of Rs 25 lakh (20 years, 9% EMIs paid by March 2025) can hope to save a total of Rs 1.37 lakh in FY2025-26 or Rs 11,461 per month. This will be through a combination of interest savings on the home loan rate reduction of 25 bps and the tac savings from higher tax slabs from April 1