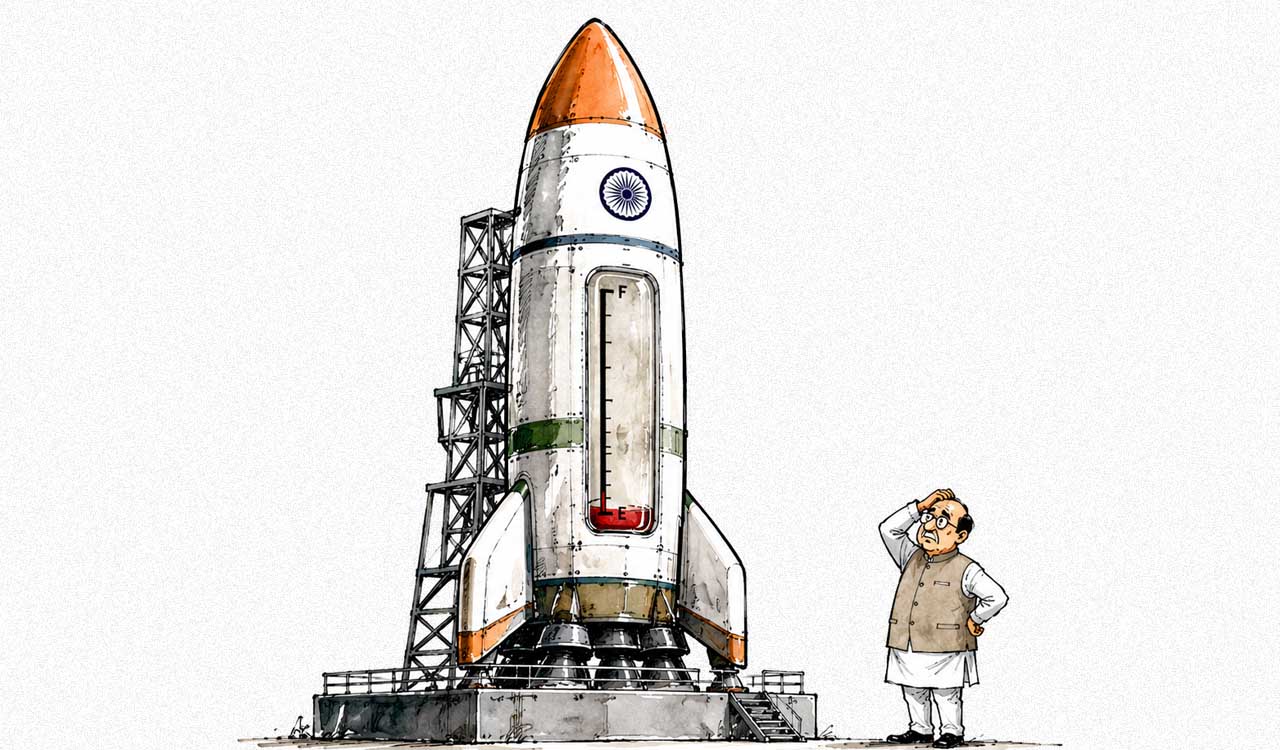

Editorial: Rooting for growth

By adopting an accommodative stance, the RBI's Monetary Policy Committee has signalled a shift in priorities from inflation containment to growth revival

The Reserve Bank of India’s (RBI) decision to cut the repo rate for the second time in a row by 25 basis points — from 6.25% to 6% — signals the need to support growth amid global turmoil and uncertainty. The Monetary Policy Committee (MPC) has changed its stance from neutral to accommodative, indicating the possibility of further rate cuts in the coming months. With the ongoing trade war, triggered by United States President Donald Trump’s whimsical tariffs, the central bank has lowered India’s GDP growth projection for FY26 to 6.5% from its earlier assessment of 6.7%. This underscores the nature of the challenges ahead. Some economists, however, expect growth to be even lower. The RBI has now projected inflation at 4% this year, down from its earlier forecast of 4.2%. It expects inflation to average 3.75% in the first half of the year and 4.1% in the second half. India is bound to feel the pain of the American tariffs, though not on the scale of other Asian economies. Goods and services exports contribute around 21% to India’s GDP, while for Thailand and Vietnam, it is much higher at 65% and 87% respectively. A positive takeaway for India is that the reciprocal tariff imposed by the US at 26% is lower than that imposed on some of the other competing countries. However, there will be a significant indirect impact as both global growth and capital flows to emerging economies are bound to decline. India’s domestic investors will also grow wary due to the ongoing global disruptions. As a result, private sector investment, which had been slowly picking up after Covid, could remain tepid in the coming quarters.

By adopting an accommodative stance, the MPC has signalled a shift in priorities from inflation containment to growth revival. On the domestic front, the slowdown in consumption and muted private investment continue to weigh on growth prospects. For borrowers, especially in the housing and auto sectors, the rate cut offers a much-needed reprieve — potentially lowering EMIs and encouraging fresh loans. However, for savers, particularly those reliant on fixed deposits, falling interest rates may erode real returns, prompting them to rethink their investment strategies. While rate cuts are a necessary tool in the monetary arsenal, it would be unrealistic to expect them to serve as a panacea for all the ills facing the economy. The central bank must remain vigilant against inflationary pressures and currency volatility that could arise from a prolonged easing cycle. Additionally, transmission of these cuts by banks to consumers remains a persistent problem. Ultimately, this rate cut sends a clear message: the central bank is willing to act preemptively to support growth. But the efficacy of this move hinges on complementary fiscal measures and structural reforms. Without those, monetary policy alone may struggle to lift the economy out of its current malaise.