Opinion: On a weak ‘note’

Various factors such as inflation, interest rates, quantum of public debt and current account deficit influence the dollar-rupee exchange rate to a great extent.

By Dr Seela Subba Rao

A heavy outflow in foreign funds from the domestic market is one of the reasons for the depreciation of the Indian rupee. Whenever the value of a currency falls, it badly impacts that nation’s economy and results in a higher rate of inflation. The demand for a currency is driven by the nation’s total imports and exports. For example, if India imports more than it exports, it raises the demand for US dollar oversupply thus resulting in a fall in the value of the rupee against the dollar.

Various factors such as inflation, interest rates, quantum of public debt and current account deficit influence the dollar-rupee exchange rate to a great extent. Political instability too matters.

Rupee depreciation, ie, decrease in the value of the rupee against the dollar, influences the current account deficit. It also puts inflationary pressures but at the same time, exports become more remunerative. Similarly, when the rupee appreciates vis-à-vis the dollar, it means the goods of our nation are more expensive, so exports will reduce.

If a country imports more than its exports, then the demand for the dollar will be higher than the supply and the rupee will depreciate.

Forex Reserves

The Reserve Bank of India (RBI)’s intervention and the dollar/rupee exchange rate are interconnected. It is pertinent to know who the market players are and how the RBI regulates them. The market players are only banks licensed by the RBI and the RBI itself. Individuals and corporates cannot enter the market. They can only deal with their respective banks. Therefore, being the regulator, the RBI dominates the market, the player and the jury. Thus, it is facile to argue that the dollar/rupee rate is ‘market determined’ and the RBI has no role in it.

Section 40 of the RBI Act, 1934, (Transactions in foreign exchange) stipulates that the Central government orders the “rate” at which the RBI shall buy or sell forex to banks (authorised persons). This “rate”, in turn, will be governed by India’s obligations to the International Monetary Fund (IMF). The dollar/rupee rate has thus been subjugated to the IMF, which is dominated by the United States from the good old days.

All the players (banks) are required to be square or near square (closing a position) in their forex positions (spot or forward) at the close of business hours each day. This ‘overnight limit’ is prescribed for each bank by the RBI. Even during the day, the prescribed ‘daylight limit’ cannot be breached. These limits are enforced by the RBI strictly.

For example, on a particular day, the RBI sells (intervenes) $2 billion in the market and one bank buys these dollars to remit them abroad for an importer (goods/services) customer. If that be the case, then the funds would have gone abroad anyway since the importer, holding an import licence, can remit funds abroad as a matter of right. So, the $2 billion forex reserves depletion is caused not because of RBI’s intervention but because of the import licence granted by the Ministry of Commerce.

Therefore, RBI’s intervention cannot deplete forex reserves. Instead, the cause of forex reserves depletion is an unimaginative import/export policy of the Ministry of Commerce without keeping the RBI in the loop. The notion that the RBI has depleted forex reserves from $642 billion to $537 billion, ie, from 8 September 2021 to 30 September 2022, by intervening (selling dollars) in India’s inter-bank forex market is manifestly incorrect. After all, the RBI is the custodian of India’s forex reserves and is responsible for managing their investments economically.

![]()

CAD Concern

The rupee’s fall these days is mainly due to high crude oil prices, a strong dollar overseas and foreign capital outflows. Finance Minister Nirmala Sitharaman recently said the Indian currency was relatively better placed than other global currencies against the greenback. She further said the RBI and the government of India keep a close watch over the developments. Current currency depreciation around the world is being triggered by geopolitical events caused by Russia’s invasion of Ukraine. It is pertinent to mention that the US Federal Reserve recently increased the interest rates and the return on dollar assets increased compared with those of emerging markets such as India.

The current account deficit, which is a shortfall between money received by selling products to other countries and the money spent to buy goods and services from other countries, is a matter of serious concern. The current account maintains a record of the country’s transactions with other nations. It includes net trade balance of goods and services, net earnings on overseas investments and payments such as remittances and foreign aid. As the current account widens, foreign capital outflows could be severe resulting in the depreciation of the rupee further. Hence, it is important to keep the current account deficit in check. It is imperative that trade control regulations (flow of goods/services), exchange control regulations (flow of funds) are administered rigorously by the RBI with due diligence.

The central bank, along with the government of India, is fighting on several fronts to slow the rupee’s decline to fresh records. The RBI has reported to have taken all steps not to allow “jerky movements” of the rupee and stressed that the Indian currency has witnessed the least depreciation in recent times. Fair productivity growth, improvement in commodity terms of trade and narrowing inflation differential will help achieve equilibrium in real exchange rate.

(The author is former Assistant General Manager, Nabard)

Related News

-

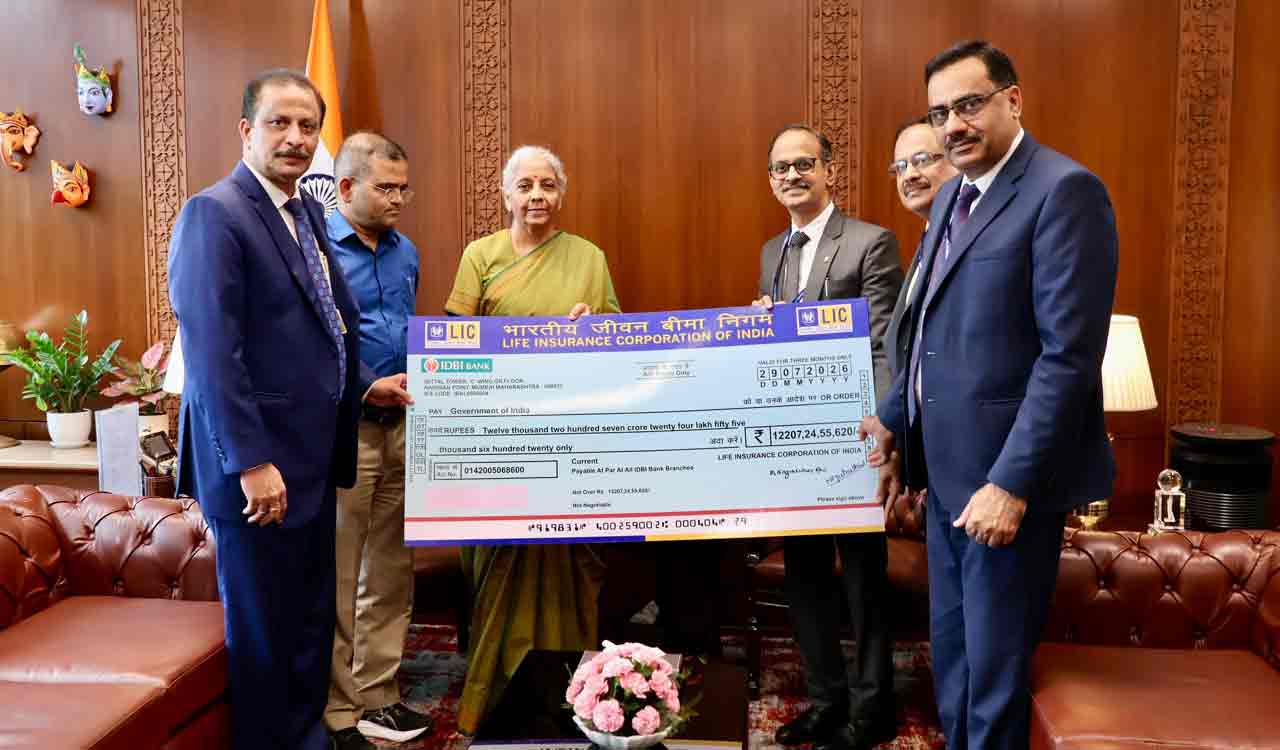

Finance Minister receives Rs 12,207 crore LIC dividend for FY 2025-26

-

Net FDI drops to USD 6.95 billion in FY26 amid higher repatriation, ODI outflows: Govt

-

Rupee jumps 61 paise against US dollar as crude oil prices fall

-

Rupee gains 28 paise against US dollar as crude oil prices tumble and global sentiment improves