Rewind: Race to be world’s factory

India recently overtook China in population. Can it repeat the feat in exports?

By AnithaRangan

Hyderabad: China replacing the United States as the world’s trading partner in the last decade is well-known while India has only chugged along. Though the India-China comparison is being done on several fronts, exports is one area where India may not impress much. Despite this, it is noteworthy that India has made great progress both in terms of trade upgradation and diversity in exporting partners.

The future does look bright and there is potential to narrow the gap with the world and China. The gap may remain but definitely will get thinner. How? Increasing lookout for diversification of global supply chains away from China and shifting of locations away from Europe due to geopolitics present an opportunity for India. This will be one of the key factors driving the structural shift in India’s exports. Support from rupee-denominated trades andpolicy initiatives to incentivise exports will add to the safety net to cushion India against possible commodity-led trade deficits in future.

Top Post

World trade in the first decade of the millennium grew at a CAGR (compound annual growth rate) of 11% (2001 to 2011) – from$6.2 trillion to $18.3 trillion. However, it slowed in the next decade to just around a CAGR of 2% to $22.3 trillion by 2021 with a fall in commodity prices and relatively benign inflation contributing to the trend. India, on the other hand,grew 21% and 3% in the same period and China at 22% and 6% respectively.

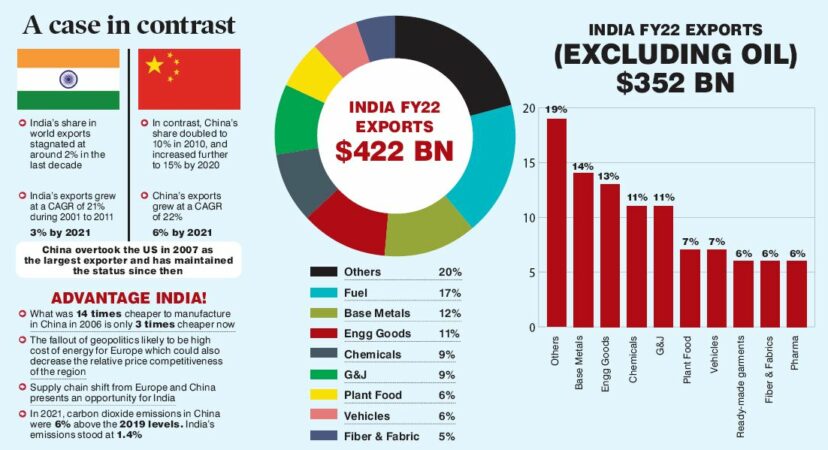

China saw a surge in exports from $250 billion in 2000 to $1.6 trillion by 2010 and further to $3.3 trillion by 2021. This took its share in world trade to 15% in 2021, more than tripling in two decades from 4% in 2001. In comparison, the combined share of the European Union is 18%. China overtook the US in 2007 as the largest exporter and has maintained that status since then.

India’s trade basket hasaltered over the last two decades. While the earlier part of the millennium was dominated by textiles and gems & jewellery, the mix has moved towards fuel, base metals, engineering goods, pharma, vehicles and chemicals. Similarly, within imports, excluding oil (which has one-third share), engineering goods have gained importance. Chemicals, metals, and plastics have also gained moderately.

However, India’s share in world exports has stagnated at around 2% in the last decade. While it grew from 0.6% to 1.6% in the previous decade, the decade leading to 2020 saw a consolidation phase. In contrast, China having after doubled to 10% in 2010, further captured a 15% share by 2020 becoming the dominant player in the global arena capturing market share from the developed world viz,the US, Europe, Japan, the UK and Canada.

Can India replicate China? While it is not easy to replicate the China model of scale and size, there is a potential to narrow the gap.

Chinks in Armour

Opportunities provided by geopolitics and/or environment compliance, and reducing labour arbitrage of China provide some low-hanging fruit favouring the shift in supply chains away from Europe and China. China and the European Union account for one-third of global trade.

- Loss in Cost Advantages

China which has traditionally been regarded as a low-cost manufacturing base appears to be under pressure due to a loss in cost advantages. Over the last two decades, average wage growth in China stood at around 14% versus average inflation of around 3%. A continued double-digit wage growth, doubling every 6-8 years, could have sustained the labour arbitrage export model at a lower base but this momentum is unlikely to sustain. In comparison, the US weekly wages over the last decade are rising by 3%. What was 14 times cheaper to manufacture in 2006 is only 3 times cheaper now. On a relative scale, is noted as ‘Holding Steadily’ due to rapid productivity growth and a depreciating currency, which have helped control costs. (BCG: How Global Manufacturing Cost Competitiveness Has Shifted over the Past Decade).

- Environmentcosts

Stricter environmental compliance on Chinese producers is having a restrictive impact on export-led industries like iron and steel, chemicals and related (plastics). In 2021, carbon dioxide emissions in China were 6% (almost 500 tonnes)above the 2019 levels. India’s emissions,on the other hand, stood at 1.4% (30 tonnes) above 2019 levels, making India more promising for companies to comply with their environmental, safety, and health standards. (Bain & Company, 2022)

- Supply chain

The EU and Europe together account for 30-35% of the total world exports. A fall-out of geopolitics is likely to be high cost of energy for Europe which could also decrease the relative price competitiveness of the region. The dominance of China which accounts for 15% of the world’s export is also coming to test as the pandemic and its long-lasting impact on China followed by geopolitics have dawned a wake-up call for the world to diversify away from China. While a supply chain shift from Europe and China presents an opportunity for India to become a key benefactor, what could be the enablers which could assist this?

Government policy support is the foremost enabler

- Production linked Incentive scheme in 13-plus sectors viz, electronics, automobiles, pharma, food processing, speciality steel and textiles (man-made fibres) could provide a medium-term boost. Three more sectors have been added viz toys, bicycles and drones. Besides, several other schemes which are aimed at creating an ecosystem for import substitution and export promotion are positive for medium-term progress. Export focus initiatives like ‘One District One Product’, monitoring the State competitiveness using an Export Preparedness Index are other focused efforts to grow exports.

- India already has 12 FTA/RTA (free/regional trade agreements) with nations with the recently concluded one with Australia. Other nations and regions include Japan, South Korea, Mauritius, ASEAN and SAARC. India has also concluded a comprehensive partnership agreement with the UAE. Notably, the merchandise exports to countries/regions with India’s trade agreements have grown 21% in five years ending FY21 (Export Preparedness Index document).

- Thrust to enhance the infrastructure from schemes like National Logistics Policy (NPL) could give the much-needed impetus to making Indian exports globally competitive by reducing logistics costs and improving the efficiency of export processes. Several facets of the NLP like the Unified Logistics Interface Platform (ULIP) that is aimed to bring all the digital services related to the transportation sector into a single portalshould make exports more competitive.

Ofcourse, not to leave out the fundamental strength of our diversified export basket.Weak global growth may have subdued the growth this year. The near-term outlook, while clouded by global slowdown pressures, also suggests that all segments have not been equally subdued. The bright spot is from industrial machinery and electronics which in aggregate is growing 25% (Apr-Jan 2023) led by smartphone exports growing around 80% while other categories are also growing between 10% and 25%. Plant food and prepared food have also risen between 10% and 25%. Auto and auto components also show promise led by structural shift. There are also prospects of rebound from iron-ore, cereal exports in the near term. While the discretionary basket may take time to rebound, the non-discretionary basket will support the downturn.

- Settlement in INR is another enabler, especially with emerging market and developing economies. Alongside this, it reduces the dependency on external capital funding of the current account deficit (CAD), the success of which again hinges on growth in exports. The rupee trade settlement mechanism, set up by the RBI in July 2022, has the potential to make strikes in promoting Indian exports by increasing global interest in the rupee with the use of special vostro accounts (account that domestic banks hold for foreign banks in the former’s domestic currency).So far, the Reserve Bank of India (RBI) has granted approvals to foreign banks in 18 countries to open vostro accounts. This includes Germany, Russia, Guyana, Israel, Kenya, Malaysia, Mauritius, Myanmar, New Zealand, Singapore andthe UK. The geopolitical conflict opened the scope to explore this route with Russia initially. The key deterrent has been that the nations with whom we have a large trade deficit like Russia would find it complex to deploy INR. Regulators in India are, however, active in finding optimum solutions. The internalisation of the rupee could be a game changer, especially with developing economies. European Central Bank President Christine Lagarderecently commented: “Euro Dollar status should not be taken for granted.” She mentions INR (along with Renminbi) setting up an alternative payment mechanism is a focal moment for India that the world is taking notice of India and its policies.

A rebound in exports is critical to our commodity-shock sensitive imports. Trade deficit has once again been a heightened focus with the Q2FY23 deficit reminiscing the 2013 episode. While reserves this time have countered the currency shock, the scale of rundown has also been a reminder that India’s CAD is funded with “borrowed reserves”. While the recent narrowing trade deficit supported by robust services has stemmed the tide for now, the safety cushions have lessened.

In summary, global trade is likely to look for new pastures with growing interest of nations to diversify supply chains away from China and Europe. This puts India in a bright spot at a time when domestic growth is also relatively resilient and government’s willingness to position India as the favoured nation is very high. Climate and environmental cost considerations are also posing India as a tough competitor. Moreover, leveraging these opportunities, many domestic and structural developments like the PLI scheme and the government’s initiatives in bolstering India’s infrastructure and logistical competitiveness is giving Indian exports the required edge in global trade. The future of Indian exports looks bright and promising!

(The author is Economist, Equirus Securities (P) Limited)

Related News

-

French Institute in India announces 35 Villa Swagatam laureates

-

Indian boxer Preeti dominates Nicole Clyde to enter women’s 54kg last four

-

Samsung to debut India-specific AI features in next Galaxy smartphone, says CEO

-

India reclaims No 1 spot in ICC Men’s T20I Team Rankings after Zimbabwe series win