Dinesh Credit Score Was 580 — Here’s How He Recovered It Using One Simple Strategy

Dinesh’s 580 (Ouch) Credit Score and the Magical Plot Twist Nobody Talks About

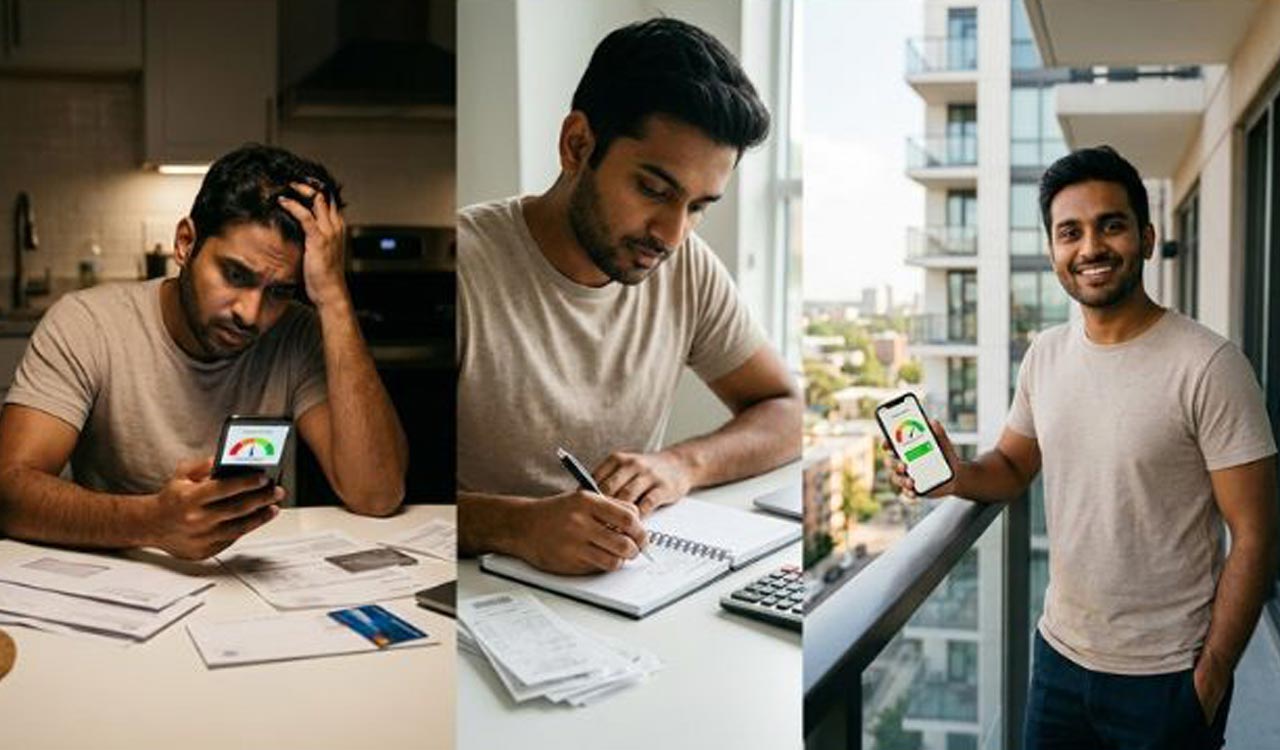

Mumbai: Dinesh never imagined his credit score would become a bigger drama than his favorite Netflix series. When his score landed at 580, friends started whispering words like “financial zombie” and “credit purgatory.”

Before Dinesh found the answer, every loan application felt like begging for extra chutney at a roadside dhaba. Then he discovered a simple strategy through LoansJagat’s credit repair product, and suddenly everything started to make sense.

This is the story of how one smart move turned his score around, and how you can learn from it.

Let us be honest. Credit scores are like reputation in school, but with real money consequences. A score at 580 is like showing up in torn jeans to a business meeting. Not fatal, but it sure sends a message, and most lenders are going to judge.

The surprising part of Dinesh’s turnaround wasn’t a secret trick or a shady loophole. It was consistency, discipline, and a smart tactical approach. Yes, that sounds boring, but in finance, boring often equals profitable.

“Wait, My Credit Score Is 580?!” The Horror That Woke Dinesh Up

Imagine waking up to the realization that your credit score is 580. For most people, that number feels like a punchline, but for Dinesh, it was an alarm bell. He needed to borrow money for a new car and a small renovation, but every lender looked at his score and shook their heads like disappointed parents.

That exact feeling was echoed in a Reddit thread where users discussed realistic strategies to improve bad credit scores. You can read it here: https://www.reddit.com/r/CRedit/comments/1l3ussa/what_are_some_proven_hacks_or_quick_strategies_to/.

Credit score recovery is not just about quick hacks or myths. It is about real strategies that work consistently over time. The Reddit thread underlines common mistakes people make and points toward solutions that actually help, just like what Dinesh eventually found.

Let’s break down how a score of 580 stacks up in real-life financial terms. Scores typically range from 300 to 900 in many systems. A score of 580 means lenders see you as risky, often resulting in higher interest rates or flat-out denials. Dinesh was paying interest rates of 24% on personal loans and 22% on credit card balances because that was all he qualified for. Those rates were bleeding his finances and keeping his credit score stuck.

Now imagine this scenario. A normal person with a credit score of 700 might qualify for a personal loan at 12% interest. For the same ₹1,00,000 loan, the lower rate saves thousands over time. That stark difference motivated Dinesh to act.

But how?

“Here’s the Real Secret No One Tells You” – The Not-So-Secret Strategy That Actually Works

Here is where the plot twist comes in. There is no credit-score fairy dust. The simple strategy Dinesh used involved three basic actions: reduce outstanding balances, avoid late payments, and strategically use credit. These might sound obvious, but the devil is in the discipline.

Dinesh started by listing every account that was dragging his score down. Credit card balances, old EMIs, and a forgotten store card that had ₹12,000 sitting on it for months. His first financial mirror moment was realizing that high balances relative to credit limits were crushing his score.

For example, if your credit card limit is ₹50,000 and your balance is ₹40,000, your credit utilization ratio is 80%. That screams risk to lenders. But if you bring that down to 30% or lower, the impact is huge. So Dinesh began paying down his cards methodically.

He shifted debts strategically, using a personal debt consolidation product from LoansJagat to combine high-interest credit card balances and small loans into a single repayment. Instead of juggling three lenders with various due dates and interest rates of 22%, 24%, and 20%, he consolidated everything into one loan at 13%.

That immediately reduced the cost of his credit and improved his payment consistency. Now let’s talk numbers. If Dinesh had:

Credit Card A: ₹40,000 at 22%

Credit Card B: ₹30,000 at 24%

Store Loan: ₹15,000 at 20%

He was paying approximately ₹2,200, ₹1,800, and ₹900 monthly respectively, totalling ₹4,900 in high-interest EMI vibes. Consolidating into a ₹85,000 loan at 13% might reduce his monthly burden to around ₹2,500, making payments manageable.

The improved cash flow reduced missed or late payments – and late payments are poison for credit scores.

Over the next three months, Dinesh focused on making every payment on time. That created a positive repayment history. His credit utilization ratio dropped from 80% to 28% as he chipped away at outstanding balances.

The credit bureaus started sending him little score bumps, like birthday cash you actually want. Six months later, Dinesh’s score was above 650. Nine months later, it crossed 700.

“So What’s the Moral of This Financial Fairy Tale?” – Discipline Beats Dashboards

Some people look for instant hacks and get-rich-quick schemes online. The Reddit thread linked above is full of hopeful strategies, some good, some less realistic. But the key takeaway is this: no amount of quick tips will replace responsible credit behavior.

The numbers do not lie. Consistent payments, lower utilization, and smart consolidation are what move the needle.

A high credit score opens doors. It means lower interest rates, better loan terms, and more financial freedom. It means lenders see you as trustworthy. And that changes your financial world.

If you are struggling with a low credit score like Dinesh once was, take a page from his book and start with a plan. Learn where your weak points are. Get a consolidated picture of your liabilities. And make a decision to change how money works for you rather than against you.

To explore tools that can help you do this, like strategically structured consolidation loans and credit management guidance, check out the LoansJagat and take the first step toward real credit transformation.

Credit may seem like a mysterious score, but your path back to financial confidence is something you can build one smart decision at a time. Your credit score is not your identity, but it is a powerful tool when you learn how to wield it.