Editorial: West Asia crisis — grim fallout for Indian economy

The closure of Strait of Hormuz, which carries nearly 20% world’s oil supply, could push up oil prices for import-dependent India, widening the current account deficit, weakening the rupee, and fuelling inflation

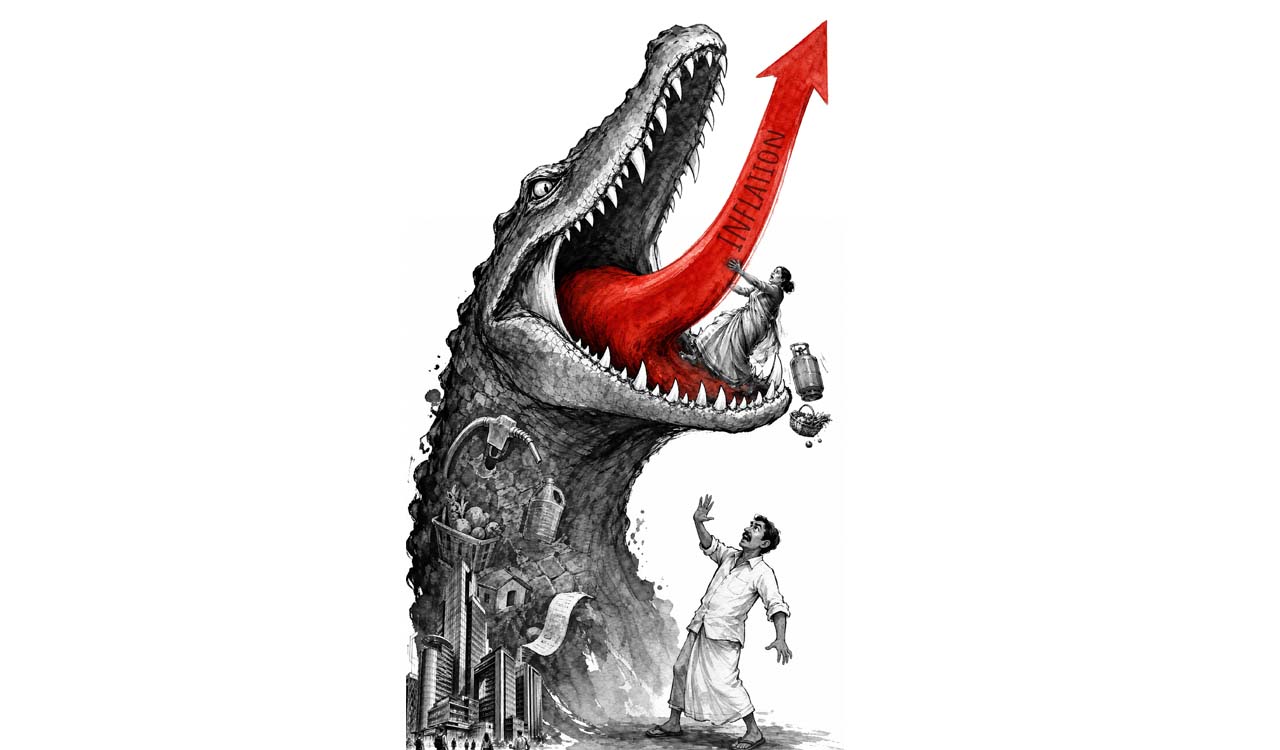

The potential economic impact of the ongoing crisis in West Asia brings back bitter memories of the Gulf War that broke out nearly three-and-a-half decades ago. While the 1991 conflict triggered a forex crisis in India, leaving the then government with no option but to initiate economic liberalisation, a radical reform that became, over time, an irreversible policy direction. This time around, the Indian economy is far more resilient, marked by strong fundamentals and a wide array of international trade options. Despite being the world’s fastest-growing large economy, India is now staring at a grim situation as the escalating conflict in West Asia, triggered by the US-Israel strikes on Iran and the subsequent retaliatory attacks by Tehran, casts a long and ominous shadow over the economy. The biggest challenge is in the energy sector. The closure of the Strait of Hormuz, which carries nearly a fifth of the world’s oil supply, could have serious repercussions for import-dependent India. Nearly 52 per cent of India’s monthly crude imports — roughly 2.6 million barrels per day — transit through the Strait of Hormuz. A sustained disruption would send India’s import bill spiralling, widen the current account deficit, and put immense pressure on the rupee. Being the world’s third-largest oil consumer, India will have to bear the brunt of the consequences of the war on Iran. In the case of liquefied natural gas (LNG), India’s cushion is much thinner, as additional LNG stockpiling is significantly more challenging than crude oil and petroleum fuels.

This is because India’s largest LNG supplier, Qatar, has also halted LNG production after a couple of its facilities were attacked by Iran. Surging crude oil prices and disrupted trade flows threaten to make imports costlier, stoke inflationary pressures, and adversely impact monetary policy. India imports nearly 80% of its crude oil requirements. A weaker rupee, rising import costs, mounting inflationary pressures and a potential recalibration of monetary policy loom large on the country’s economic landscape. Whenever the rupee falls against the US dollar, the immediate casualty is the oil import bill. The burden slowly shifts to businesses and households, pushing up inflation and eroding purchasing power. A $1 rise in crude oil increases India’s annual import bill by roughly $1.5–2 billion, depending on total import volumes. This directly widens the current account deficit (CAD), which has increased to $ 13.2 billion, amounting to 1.3% of the GDP, in the third quarter of 2025-26, up from $11.3 billion in the same period last year. Though the export-oriented information technology sector may gain from the weakening rupee, it has been grappling with slower client spending and the disruptive churn triggered by rapid advances in artificial intelligence. Another area of concern is the safety and security of nearly 10 million Indian migrants spread across the Gulf region.