Gold, Gulf, and the Rupee

India has weathered economic storms before. The question is whether it will meet this one with the same seriousness

By Burra Naga Trinadh

In the winter of January 1998, South Korean housewives queued outside banks clutching wedding rings and family heirlooms – not to sell them, but to donate them to their country. Within months, 3.5 million citizens had surrendered 227 tonnes of gold, raising $2.2 billion to help repay an IMF bailout during the 1997 Asian Financial Crisis. South Korea cleared that debt three years ahead of schedule. Koreans today call it one of their proudest national moments.

In 1973, when OPEC’s embargo quadrupled oil prices overnight, Britain imposed a three-day working week and asked citizens to heat only one room. The United States enforced a mandatory 55 mph speed limit purely to cut fuel consumption. Japan launched sweeping national conservation drives. These were not acts of governmental weakness. History called them responsible.

India has faced its share of storms too. The question, as always, is whether it will meet this one with the same seriousness.

When Prime Minister Modi stood before a public gathering at Secunderabad on May 10 and asked Indians to pause gold purchases, avoid foreign holidays, carpool, and work from home, the reaction was predictable — ridicule, political theatre, and jewellery stocks crashing 11 per cent overnight. Congress leader Rahul Gandhi called it “proof of failure.”

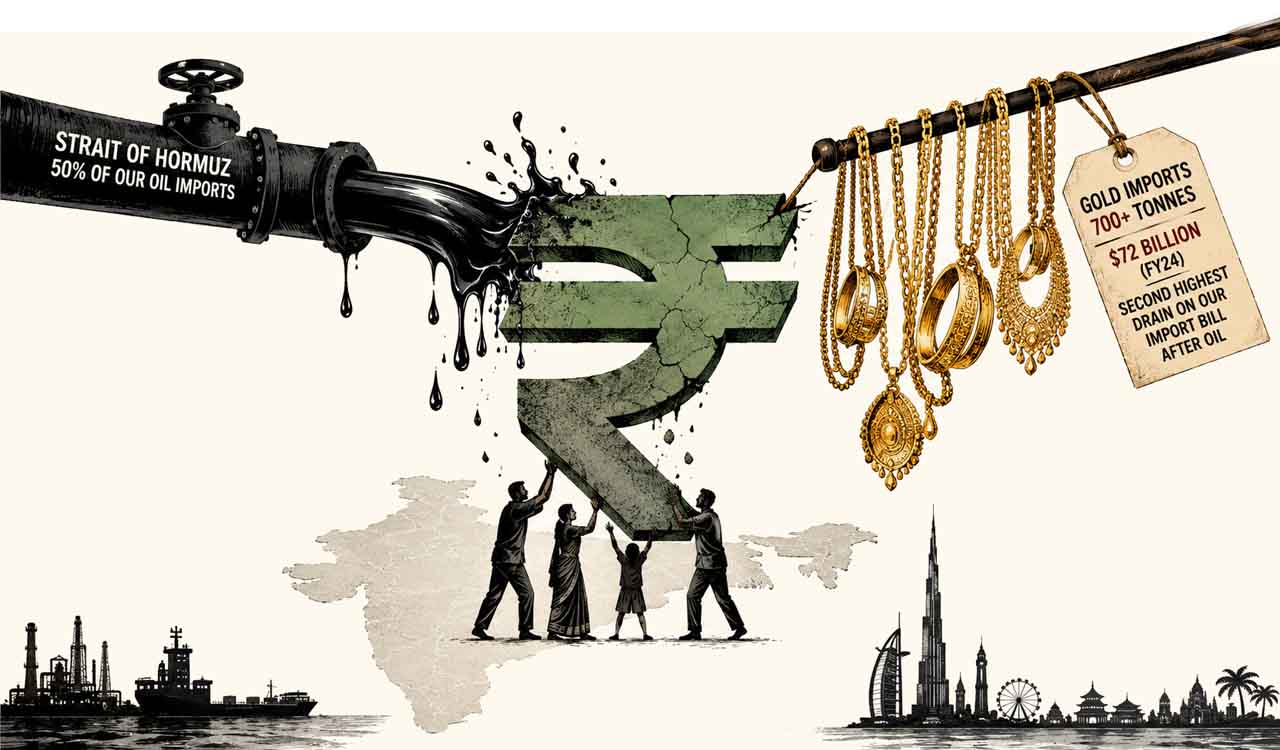

But strip away the politics, and what remains is a policy message of remarkable clarity, one that every Indian household would do well to understand before dismissing it. This is not about frugality as virtue. This is about the survival of India’s foreign exchange reserves in the face of a gathering storm. India’s forex reserves stood at $690 billion as of May 1, down $38 billion from $728 billion in late February, a fall of over 5 per cent in just two months. The IMF projects our current account deficit will reach $84 billion this year.

Crude Oil

This crisis originates from the Strait of Hormuz – this route alone carries 50 per cent of our crude imports, 60 per cent of our LNG, and virtually all our LPG. With the Iran-US confrontation keeping the Strait on a knife’s edge, Brent crude has settled above $104 per barrel. India imports 85 per cent of its fuel needs.

Last fiscal year, we spent $174.9 billion on crude and petroleum products – 22 per cent of our total import bill. We cannot simply shop elsewhere. The geography of oil is not forgiving.

Every dollar that leaves India for oil, for gold, for a holiday in Dubai comes directly from reserves. When those reserves deplete faster than they are replenished, the rupee weakens. When the rupee weakens, oil costs more in rupee terms. When oil costs more, fertilizers, medicines, and airline tickets follow. India is already standing at that inflection point.

Gold

Now consider gold. While we produce less than two tonnes domestically, India remains the second highest consumer of gold in the world. We imported over 700 tonnes last year at nearly $72 billion, the second-largest drain on our import budget after crude oil. Every gram of imported gold purchased today is a dollar less available for the energy security of tomorrow.

On foreign tourism, 32.7 million Indians travelled abroad in 2025, spending over $31 billion in foreign exchange. Aspiration is not the enemy — rising prosperity is a story worth celebrating. But in a year when every dollar is under pressure, the travelling class is being asked whether this is the year for Bali, or the year for Bodh Gaya.

On work-from-home and carpooling, the logic is linear. Fewer kilometres driven means fewer litres consumed, which means fewer barrels imported, which means fewer dollars leaving the country. EVs charged from the domestic gridsubstitute imported energy with domestically generated electricity. Multiplied across 1.4 billion people, these are not gestures. They are a measurable reduction in demand at precisely the moment demand is most expensive.

What Prime Minister Modi has done is something most elected leaders globally are too cautious to attempt. He has spoken plainly about what the numbers say. He has asked for voluntary cooperation from his citizens. The Koreans answered that call in 1998. Britain and America answered it in 1973. This is India’s version of that moment.

The Prime Minister can appeal. Governments can set policy. Central banks can defend the rupee. But national resilience has never been built in the corridors of North Block. It has always been built in homes, in markets, in the quiet daily choices of ordinary people who decided that their country was worth a small personal sacrifice. Janata Janardhan Hain.

(The author is an alumnus of the Lee Kuan Yew School of Public Policy, National University of Singapore.)

Related News

-

From Cowrie to Crypto: 5,000 years of money—one trick that destroyed every system

-

National Doctors’ Day 2026: The challenges facing India’s medical profession

-

The forgotten tradition of Telangana’s Soma drink

-

Union Minister’s murder case remains unresolved even after 50 years — a stain on India’s justice system