Editorial: Going digital

India’s digital finance system has taken a big leap forward with the Reserve Bank of India (RBI) rolling out the first pilot digital currency or e-rupee but concerns over privacy issues remain unaddressed. In the first phase, the wholesale version of the digital currency has been launched with the participation of nine banks while the […]

India’s digital finance system has taken a big leap forward with the Reserve Bank of India (RBI) rolling out the first pilot digital currency or e-rupee but concerns over privacy issues remain unaddressed. In the first phase, the wholesale version of the digital currency has been launched with the participation of nine banks while the retail e-rupee, which will have a bearing on the common man, will be ready for launch within a month. For all practical purposes, the Central Bank Digital Currency (CBDC) will be equivalent to cash. It is expected to complement the current plethora of digital payments but not cannibalise them. Since CBDC systems will allow governments and intermediaries to have access to personal data, it raises privacy concerns. In the absence of a robust data protection law, the need for data protection and governance standards in designing and implementing a CBDC will be critical. While the concept note, released by the central bank, emphasises privacy principles, it does not enumerate the principles that will form the basis for the CBDC design. The RBI needs to balance the need for privacy protection while ensuring adequate supervision for protecting the financial integrity of transactions. In the proposed model, the retail customers would hold their CBDC with intermediaries — banks — through a wallet. Banks would be responsible for ensuring the supply of CBDC on demand to consumers. CBDCs need to be integrated into the payments system of India such as UPI and digital wallets.

The interoperability between these payment systems would be vital for the success of the digital economy. Since CBDCs will use cryptography, it will render the system safer as compared to the existing payment infrastructure. To create an enabling legal framework for CBDCs, amendments to existing laws such as the RBI Act,1934, Coinage Act, 2011, Foreign Exchange Management Act, 1999, and Information Technology Act, 2000, may be necessary. Digital currencies are increasingly gaining traction across the world with as many as 105 countries currently exploring different models of digital currencies. What makes the RBI’s digital currency different from the conventional rupee when it is transacted digitally is that it is based on blockchain technology. This lends CBDC transactions a level of transparency and security that surpasses even the existing digital security of India’s banking system. In her Budget speech, Finance Minister Nirmala Sitharaman had announced that the RBI would issue a digital currency this year to give a big boost to the digital economy. The central bank has been pursuing CBDC’s launch to counter perceived threats posed by cryptocurrencies to financial stability. Hopefully, the e-rupee will help bolster India”s digital economy, enhance financial inclusion and make monetary and payment systems more efficient and transparent. However, in a country where cash remains the king, digital currency cannot replace physical notes.

Also Read

Related News

-

PM Modi chairs high-level meeting to review West Asia crisis impact on India’s energy security

-

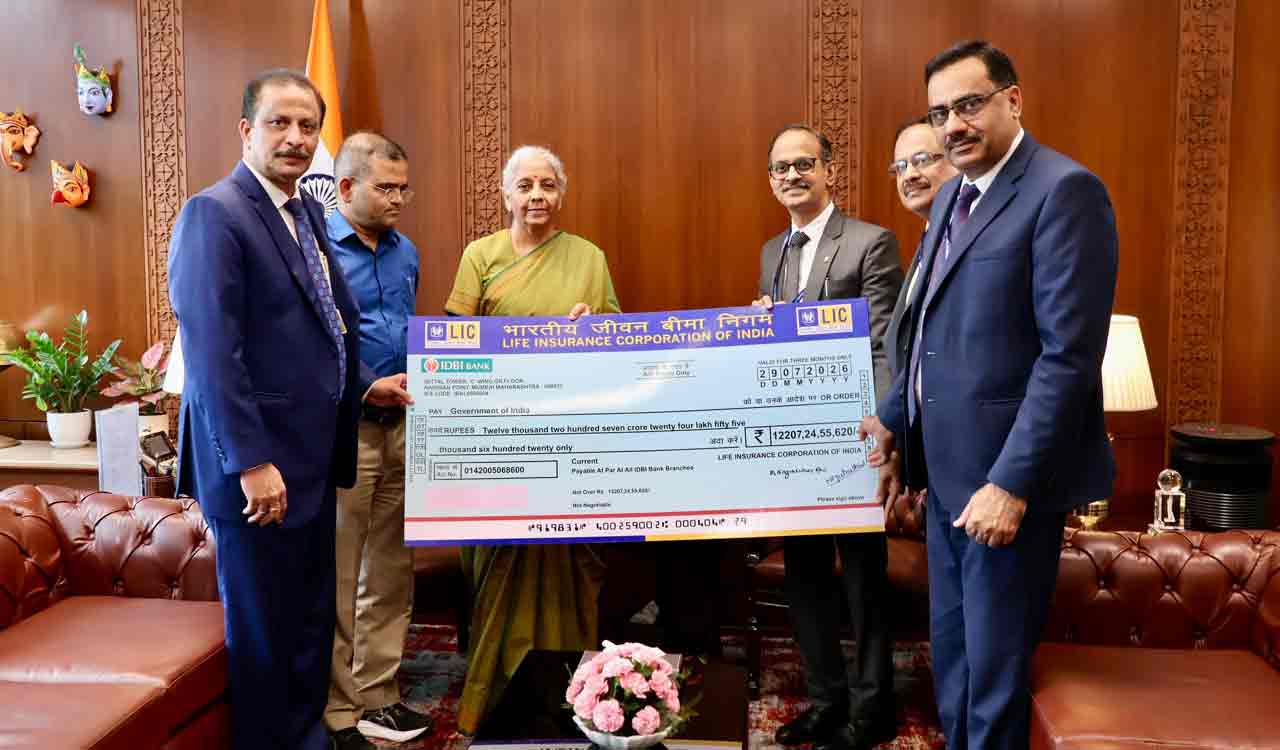

Finance Minister receives Rs 12,207 crore LIC dividend for FY 2025-26

-

Nirmala Sitharaman asks Income Tax officials to serve citizens better

-

She is a fool: Sanjay Raut attacks Nirmala Sitharaman over student paper leak comments