Editorial: Withdraw GST on insurance

The tax imposes an unfair burden on policyholders and runs contrary to the intent behind incentivising these policies

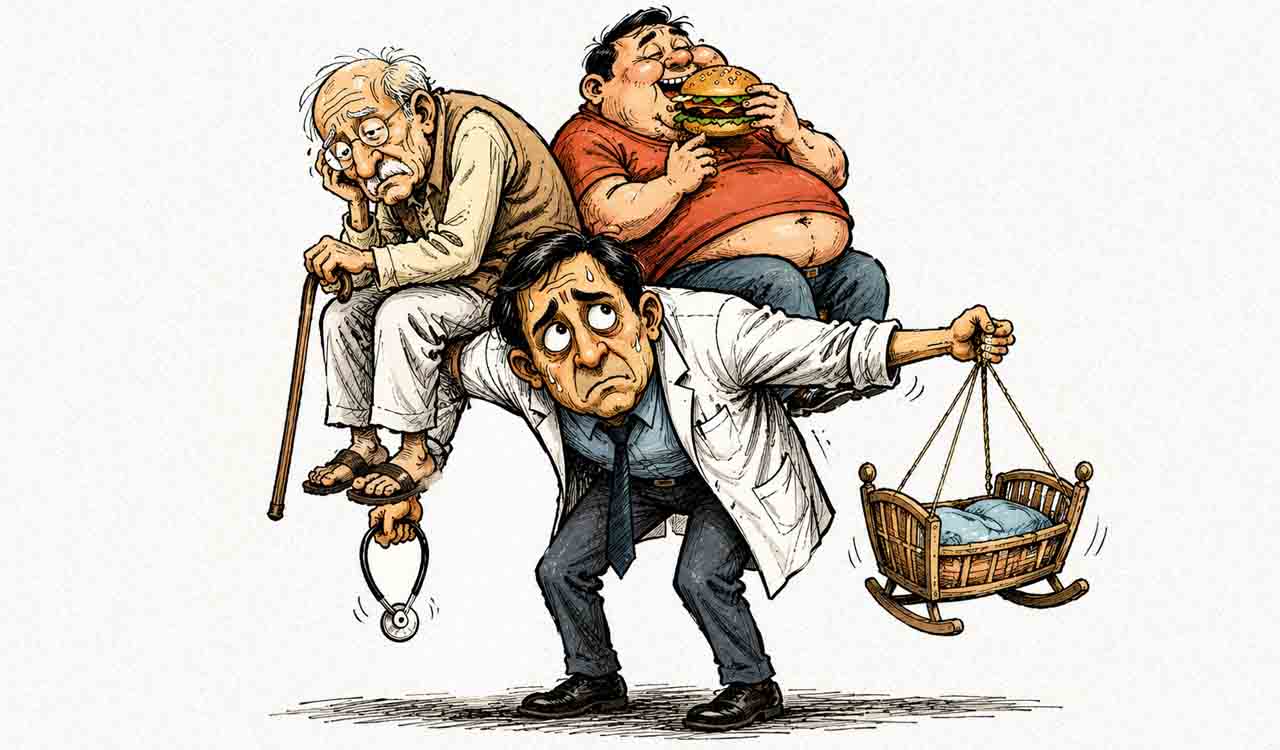

In a country where health insurance penetration is abysmally low, levying an 18% Goods and Services Tax (GST) on life and medical insurance premiums is totally unfair and stifling. While seeking its immediate withdrawal, the Union Minister of Road Transport and Highways Nitin Gadkari has rightly observed that the move amounted to levying tax on the uncertainties of life. In a letter to his colleague and Finance Minister Nirmala Sitharaman, he said the high taxation on medical insurance premiums would prove to be a deterrent for the growth of this segment of business which is socially necessary. A person who covers the risk of life’s uncertainties to give protection to the family should not be levied tax on the premiums to purchase cover against this risk. The insurance industry has long advocated for a reduction in GST to enhance the appeal of its products. Lowering the GST rate would not only make insurance more affordable but also stimulate its uptake, contributing to broader financial security and health coverage. This tax imposes an unfair burden on policyholders and runs contrary to the intent behind incentivising these vital policies. Insurance is fundamentally a tool for managing life’s uncertainties. Levying a hefty tax on premiums is especially troubling for the vulnerable sections who already find it challenging to afford adequate coverage. Such stifling measures may adversely affect the quality of healthcare, particularly at a time when the participation of the private sector in improving health infrastructure and services needs to go up significantly.

The tax on insurance in India is among the highest in the world. The impact could have a detrimental effect on the accessibility and growth of insurance products. This is particularly pertinent given the fact that insurance is more of a ‘pull’ product — consumers need to be drawn to it — rather than a ‘push’ one. As per the IRDAI’s (Insurance Regulatory and Development Authority of India) data for 2022-23, insurance penetration in India is around 3.2% of the GDP for life insurance and 0.94% for health insurance. The average percentage of renewal of retail health insurance policies is in the range of 65% to 75%, indicating that a large number of policyholders are unable to pay the premium due to frequent hikes in insurance premiums and high GST rates. Moreover, the current taxation policy is inconsistent with the government’s broader objective of promoting social welfare and economic stability. By removing the GST on insurance premiums, the government can take a significant step towards ensuring that more citizens are protected against life’s unpredictability without additional financial strain. The government must heed Nitin Gadkari’s call. There may have been political differences between Gadkari and Prime Minister Narendra Modi but they must be set aside on this vital fiscal policy issue. In fact, the Parliamentary Standing Committee on Finance too had recommended a reduction of GST on health insurance.