Opinion: BRICS’ quiet challenge to the dollar

BRICS nations’ push to trade in local currencies reflects frustration with dollar dominance and signals a shift in the global monetary order

By Dr Jadhav Chakradhar, Prof Mini Thomas P

As geopolitical tensions rise, substantial changes are quietly reshaping the world’s monetary system. A classic example is the US imposing high tariffs on several Indian products in August because of India’s oil trade with Russia. Developments like this show how politics and trade are now intricately linked, slowly changing how global finance works.

Also Read

For decades, the US dollar has reigned supreme as the world’s reserve currency, facilitating seamless international trade and payments. However, the BRICS bloc — Brazil, Russia, India, China, and South Africa — , which has now expanded to include five more new members, is increasingly challenging this dollar hegemony by promoting trade in local or national currencies and exploring alternatives. This push toward de-dollarisation, while still nascent, reflects broader frustrations with dollar dominance and could reshape global economic dynamics. As intra-BRICS trade in non-dollar currencies approaches 50 per cent in 2025, its implications for trade, reserves, and stability are immense.

The modern international trade system operates through a network of interconnected financial institutions, where currencies serve as units of account, means of payment, and stores of value. Most cross-border transactions are settled via the SWIFT (Society for Worldwide Interbank Financial Telecommunication) system, with banks maintaining correspondent accounts (vostro or nostro) in foreign jurisdictions to facilitate transfers. A key feature is the use of “vehicle currencies”, which are intermediary currencies like the dollar or euro that bridge trades between non-convertible or less liquid currencies.

Dollar’s Ascent

The dollar’s acceptance as the global currency of trade stems from its liquidity, stability, and access to the vast US financial markets. Oil, commodities, and many goods are priced and invoiced in dollars, creating a self-reinforcing cycle. For instance, even trade between India and Russia traditionally requires converting Indian rupees to US dollars, then US dollars to Russian rubles, incurring costs and risks. This double conversion exposes participants to exchange rate volatility and US monetary policy spillovers, as highlighted in IMF analysis.

The dollar’s ascent began post-World War II with the Bretton Woods Agreement of 1944, which pegged currencies to the US dollar, which itself is convertible to gold at USD 35 per ounce. The US, emerging as the world’s largest economy with sound financial infrastructure, provided stability amidst global reconstruction. The system formalised in the Bretton Woods Agreements Act (1945) established the IMF and World Bank, with the dollar as the anchor. The 1971 Nixon Shock ended dollar-gold convertibility, but the petrodollar system solidified its dominance.

A BRICS currency or enhanced local settlements offers benefits: lower transaction costs (up to 30 per cent savings via direct swaps), reduced exposure to dollar volatility (eg, rupee-ruble trading shielded from dollar swings), and greater financial autonomy

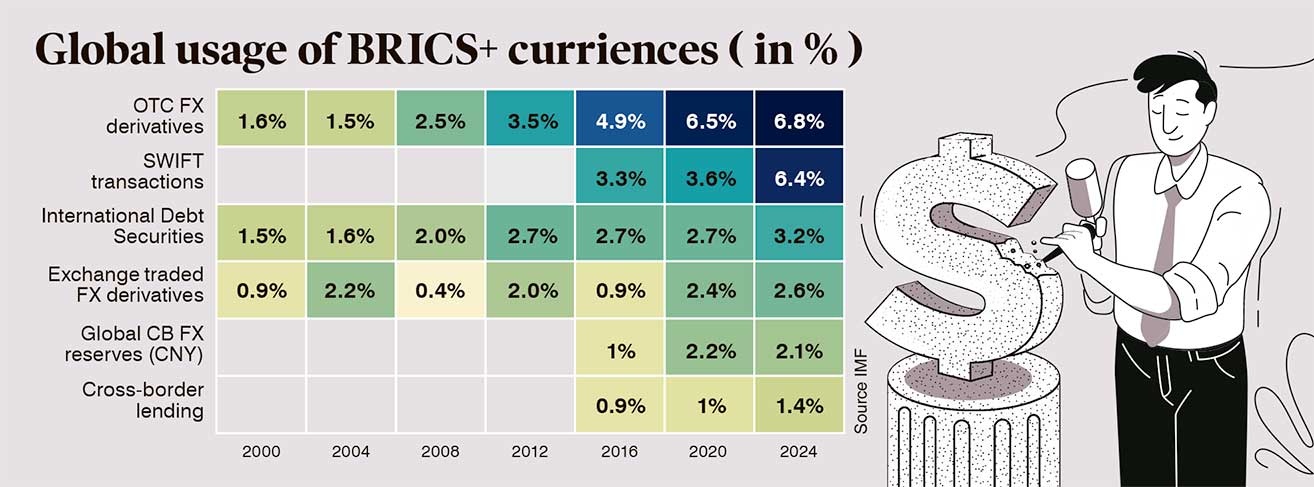

In the 1970s, amid oil supply shocks, OPEC nations agreed to price oil in dollars and recycle revenues into US assets, as detailed in IMF studies on petrodollar recycling. This created demand for dollars, funding US deficits while providing liquidity. By the 1980s, deregulation and globalisation entrenched the dollar: it now accounts for 88 per cent of foreign exchange transactions, 60 per cent of global debt, and 59 per cent of international reserves, as per BIS and IMF data.

Seeking Alternatives

BRICS nations, representing 40 per cent of global GDP (in purchasing power parity terms), are diversifying due to geopolitical risks and economic policy uncertainties. US sanctions on Russia post-2022 Ukraine invasion froze USD 300 billion in reserves, exposing vulnerabilities. Similar pressures on Iran and Venezuela highlight how dollar weaponisation can disrupt trade. China, facing US tariffs, seeks renminbi (RMB) internationalisation to reduce currency exposure.

The Reserve Bank of India (RBI) introduced a framework in July 2022 for international trade settlements in Indian Rupees (INR), enabling invoicing, payments, and settlements for exports/imports with partner countries using Special Rupee Vostro Accounts (SRVAs). This applies broadly to any trading partner but was initially highlighted for key bilateral deals with countries like Russia (eg, for energy imports) and Sri Lanka (eg, for credit lines and essential goods), amid efforts to reduce dollar dependency and circumvent sanctions-related SWIFT restrictions.

A BRICS currency or enhanced local settlements offers benefits: reduced transaction costs (up to 30 per cent savings via direct swaps), mitigated dollar volatility (eg, rupee-ruble trading shielded from dollar swings), and enhanced financial autonomy. Intra-BRICS trade, at USD400 billion in 2024, could grow faster without conversion fees, boosting further economic integration. For India, INR settlements with the UAE and Russia have stabilised energy imports. However, BRICS currencies lack full convertibility; the RMB, comprising 2-3 per cent of global payments, faces capital controls. Volatility — eg, the ruble’s 2022 plunge — could deter adoption. No single BRICS currency dominates; a basket might fragment liquidity. Geopolitical rifts within BRICS nations (eg, India-China tensions) also hinder unity. A hasty shift risks inflation or trade disruptions, as seen in past failed experiments such as the ruble zone post-USSR.

Amid de-dollarisation, central banks are stockpiling gold as a hedge. The World Gold Council’s 2025 survey (covering 73 central banks) reveals that 43 per cent plan to increase their gold reserves in the next year, a record, with none anticipating declines. BRICS nations again lead in this emerging trend: China added 200 tonne of gold in 2024-25, Russia 150 tonne, and India 100 tonne. Global central bank purchases hit around 1,000 tonne annually since 2023, up from 400-500 tonne pre-2020.

Intra-BRICS Currency Trade

Intra-BRICS trade in their national currencies has surged, reaching around 50 per cent by mid-2025, from 20-30 per cent a decade ago. The RMB leads at 50 per cent of settlements, expanding beyond Asia, as per IMF’s 2025 paper on currency invoicing. Russia-China trade is 90 per cent non-dollar; India-Russia oil deals are denominated in rupees.

BRICS+ expansion amplifies this, with projections for 70 per cent local settlements by 2030 if systems like BRICS Pay launch. Yet, dollar dominance persists globally (47 per cent payments), with BRICS currencies having a combined share under 5 per cent. Challenges include settlement imbalances and no mandated vehicle currency. Research shows that intra-BRICS trade reduces USD reserve shares, and it correlates with geopolitical distance.

De-dollarisation is gradual, not revolutionary. Benefits like cost savings and resilience are compelling but concerns over stability temper enthusiasm. Rising gold reserves underscore diversification, potentially eroding USD dominance over decades. For BRICS, success hinges on infrastructure like CIPS (Cross-Border Interbank Payment System) expansions and currency convertibility reforms. Globally, this could foster multipolarity but risks geo-economic fragmentation if uncoordinated. Policymakers must balance innovation with stability to avoid disorderly transitions to a new international economic order.

(Dr Jadhav Chakradhar is Assistant Professor of Economics, Centre for Economic and Social Studies (CESS), Hyderabad. Mini Thomas P is Associate Professor, Department of Economics and Finance, Birla Institute of Technology & Science (BITS) Pilani, Hyderabad Campus)