Opinion: Is FDI equity inflow helping?

If we compare FDI equity inflow with China, we still fail to attract a significant share of world FDI mainly due to lack of institutional framework

By Dr Kedar Vishnu, Prof Ruchika Rai, Aditi Wani

The existing theories on foreign direct investment (FDI) emphasise capturing the reasons for the shift of investment by international firms from developed to developing countries. Earlier Classical trade theories recognised the comparative advantages of host countries as the main determinant of FDI. Further, internalisation theories on FDI argue that international firms would be interested in developing their own internal markets in developing countries to reduce the production and transaction costs they incur. As a result, they shift their operations from developed to developing countries.

Also Read

By attracting foreign capital and expertise, FDI contributes to increased investment, job creation and technological advancements in developing countries. It facilitates the transfer of advanced technologies and best practices, spurring innovation and productivity gains in domestic industries.

The Indian economy registered significant growth after Covid and is set to become the fifth-largest economy for the financial year 2023-24. Economists argue that FDI is one of the crucial drivers for this growth. Undoubtedly, it played a vital role in the 2010s and 2020s decades. However, the pandemic has drastically changed the scenario of FDI for many developing countries like India. Hence, two important questions need further investigation. To what extent has FDI helped boost our manufacturing sector and the economy after Covid-19? Is there any recent change in the priority of FDI allocation towards the much-needed manufacturing industries?

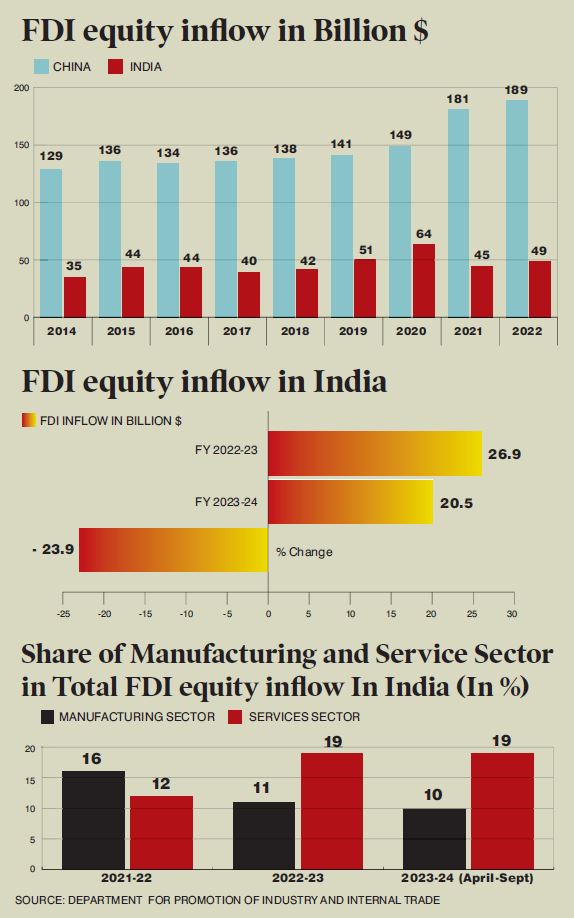

The FDI equity inflow to India enormously increased to $49 billion in 2022 from just $4 billion in 2000. India attracted 3.8% of the world’s FDI (equity) in 2022, compared with 0.3% in 2000. However, recent data has raised some major concerns about the FDI equity inflows, which declined by 24% and reached $20.5 billion in the first half of FY24 as compared with the first half of FY23 (Source: Department for Promotion of Industry and Internal Trade). So far, policymakers are not clear about the continuous decline of the FDI over the last six months.

The FDI equity inflow to China increased to $189 billion in 2022 from $41 billion in 2000, accounting for 14.6% of the world share. In India, it has risen mainly from 2005, reaching highs up to 2008, and then started declining till 2012 due to the financial crisis. The government made enormous efforts to increase the FDI inflow in 2012, and as a result, it significantly increased up to 2019. However, this increase was only for a few years as it declined again in 2023. In the case of China, the FDI equity inflow continuously increased since 1991 without much fluctuation.

Covid-19 has pushed us to face two crucial problems: the declining share of India’s worldwide FDI equity inflow in recent years and a shift in the allocation of FDI from more productive (manufacturing) sectors to less effective (service) sectors.

Shift in Sector

The allocation of FDI equity inflow for the service sector has almost remained unchanged but its contribution has significantly declined for the much-needed manufacturing sector in the first half of FY24 as compared with FY23. The decline in manufacturing share by around 6.8% in the first half of FY24 as compared with FY22 shows that we may not be able to boost our manufacturing industry productivity significantly as compared with the earlier period. This is going to be a major concern for policymakers for increasing our expenditure for capital purposes.

Our analysis of the top recipient sectors in the first half of FY24 shows that FDI allocation significantly declined for computer software & and hardware by 8.7%, followed by trading by 5.9%, drugs and pharmaceuticals by 3.9%, chemicals by 2%, automobile industry and telecommunications sectors by less than 1% as compared with FY23. However, at the same time, the contribution has significantly increased for construction activities by 8% and metallurgical by 0.4%.

Developing countries like India have struggled to boost the manufacturing sector mainly due to a lack of capital availability. Ensuring that the FDI is distributed fairly across the economy is critical to boosting overall economic growth.

No Institutional Framework

If we compare the FDI equity inflow with China, we still fail to attract a significant share of world FDI mainly due to a lack of institutional framework. So far, we have not been able to improve our government efficiency significantly, which can be understood from the governance indicator data of the World Bank. The ‘Rule of Law’ index declined from 0.3 in 2000 to 0.1 in 2022. The ‘Rule of Law’ index refers to how much people believe in and follow social norms, particularly regarding the reliability of the police, courts, property rights and contract enforcement.

Similarly, the voice and accountability index declined from 0.4 in 2000 to 0.1 in 2022. Perceptions of a nation’s citizens’ ability to choose their government, as well as their freedom of expression, etc, are captured by voice and accountability.

We have not been able to improve the political stability index significantly either. India’s political stability index value showed a meagre improvement from -1 in 2000 to -0.6 in 2022. The control of corruption index increased from -0.4 in 2000 to -0.3 in 2022, and the government effectiveness index improved from -0.2 in 2000 to 0.4 in 2023. India could attract more FDI only if we improve our institutional mechanism.