Opinion: Long road to recovery

By Dr K Srinivasa Rao The geopolitical storm due to the war between Russia and Ukraine overwhelmed the revival of the economy from the pandemic. Some early signs of data on high-frequency indicators provide the comfort of reaching the pre-pandemic levels except in the high contact industry. However, the loss of productivity has been immense […]

By Dr K Srinivasa Rao

The geopolitical storm due to the war between Russia and Ukraine overwhelmed the revival of the economy from the pandemic. Some early signs of data on high-frequency indicators provide the comfort of reaching the pre-pandemic levels except in the high contact industry. However, the loss of productivity has been immense in the two years and the ongoing third year FY23.

Since the pandemic struck, the Reserve Bank of India (RBI) has been unveiling conventional and non-conventional measures to provide support. The government has been equally proactive to provide multiple stimulus packages and articulated a long-term strategy of ‘Atmanirbhar Bharat’. Garib Kalyan Yojana has provided free foodgrains to the poor and subsidies were routed through banks to the vulnerable sections of the population.

The RBI recently released an interesting Report on Currency and Finance-2021-22 (RCF22). It provides deep insights based on actual experience with the pandemic, research and empirical analysis on the mechanics of how the economy suffered and how it may evolve, as a way forward highlighting its interlinkages taking the foreseeable factors into account. The RCF22 has an appropriate theme – ‘Revive and Reconstruct’.

Colossal Output Losses

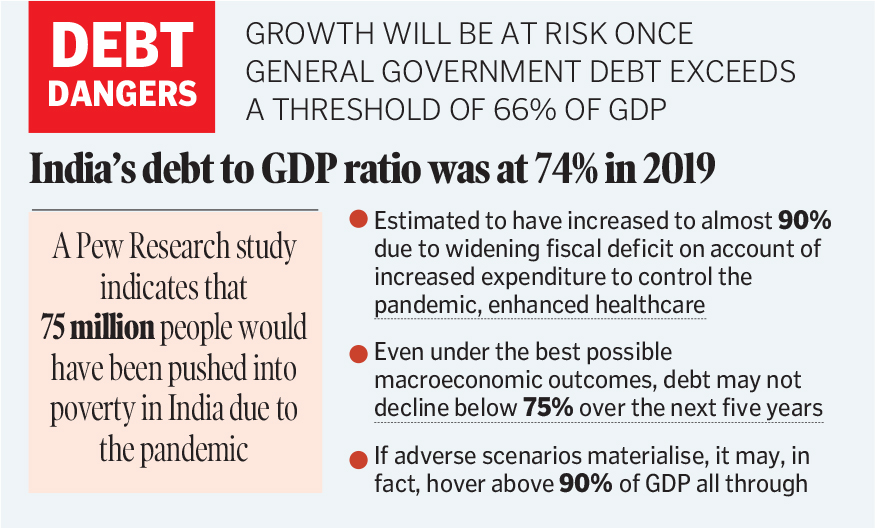

It draws the attention of policymakers to the kind of damage to the economy that cannot be factored in data points. The RBI quantified the output losses during the pandemic period at Rs 19.1 lakh crore, Rs 17.1 lakh crore and Rs 16.4 lakh crore during FY21, FY22 and FY23. Still, there could be some loss of output that could not be accounted for. There were some permanent losses of traction in enterprises that cannot be exactly quantified. Some units may not reopen, some may run on low capacity and many may lose the skills to undertake business due to psychological distress in the families — loss/sickness of near and dear. A Pew Research study indicates that 75 million people would have been pushed into poverty in India due to the pandemic.

The RFC22 observed that due to the pandemic stress, the GDP nosedived to minus 6.6% in FY21, recovered to 8.9% for FY22 and is likely to grow at 7.2% for FY23, taking the GDP growth to 7.5% beyond FY23. The recovery of the economy from the pandemic shock may stretch to as far as 2034-35. The geopolitical stress has exacerbated the risks to recovery. It is not enough if the high-frequency parameters are restored to pre-pandemic levels. There is more to recovery beyond these measured parameters.

Risks to Economy

The actual and projected outlook on the economy and inflation is reflective of volatility hit more by the supply side disruptions and rising oil prices to a new high. It will feed into CPI/WPI not only in India but across the globe warranting action from central banks. Even after the rate hike of 40 basis points and CRR edging up by 50 basis points, the RBI has not altered its outlook on the GDP that stays at 7.2% for FY23 and average inflation tilted towards the upper edge of the target at around 5.7%. Expecting a further rise in inflation and rate hike by Federal Reserve, the RBI held an off-cycle monetary policy committee meeting to announce big bang measures to support growth while fighting inflation.

It can be observed that the International Monetary Fund (IMF) has revised down its forecast of global output growth for 2022 by 0.8 percentage points to 3.6%, in a span of less than three months. The IMF projects inflation to increase by 2.6 percentage points to 5.7% in advanced economies in 2022 and by 2.8 percentage points to 8.7% cent in emerging market and developing economies. The upside signals of inflation are glaring and clear.

The World Trade Organization (WTO) has scaled down the projection of world trade growth for 2022 by 1.7 percentage points to 3%. Now the major risk comes from the external sector due to the war and lingering Covid19 in some parts of the world. The IMF brought down its GDP projections for FY23 from 9% to 8.2%, while World Bank from 8.7% to 8%.

Challenges in Revival

The near-term challenges include absorption of surplus liquidity. The RCF22 further hints that every percentage point increase in surplus liquidity above 1.5% cent of Net Demand and Time Liabilities (NDTL) of banks could cause average inflation to rise by 60 basis points in a year.

It also observed that growth will be at risk once general government debt exceeds a threshold of 66% of GDP. According to the IMF, India’s debt to GDP ratio was at 74% in 2019, a notch more than the trigger point even prior to the pandemic. It is now estimated to have increased to almost 90% due to a widening fiscal deficit on account of increased expenditure to control the pandemic, and enhanced health and vaccination expenditure.

According to the RCF22, even under the best possible macroeconomic outcomes, general government debt may not decline below 75% of the GDP over the next five years. If adverse scenarios materialise, debt may, in fact, hover above 90% of the GDP all through. A medium-term strategy of debt consolidation aimed at reducing debt to below 66% of the GDP over the next five years is, therefore, important to secure India’s medium-term growth prospects.

Taking a cue from the RFC 22, market participants should be prepared for a long-haul resuscitation of the economy spread over a number of years. According to the report, durable economic revival will hinge on seven strategic pillars — aggregate demand; aggregate supply; institutions, intermediaries, and markets; macroeconomic stability and policy coordination; productivity and technological progress; structural conditions; and sustainability. All stakeholders will have to work in coordination to pull the economy from the pandemic-induced abyss and erase the scar.

(The author is Adjunct Professor, Institute of Insurance and Risk Management (IIRM), Hyderabad. Views are personal)

Now you can get handpicked stories from Telangana Today on Telegram everyday. Click the link to subscribe.

Click to follow Telangana Today Facebook page and Twitter .