Banking on privatisation

The very purpose of nationalisation in India — serving the unbanked and under-banked — is yet to be achieved and financial inclusion cannot afford the luxury of complete privatisation

By B Yerram Raju

Banking in India has a transformational history in tune with the requirements of the economy. Currently, the transformation envisages the re-emergence of private banks with the change in licensing policy towards that end.

McKinsey anticipates that the pandemic will present a two-stage problem for banks. “First will come severe credit losses, likely through late 2021; but almost all banks and banking systems are expected to survive. Then, amid a muted global recovery, banks will face a profound challenge to ongoing operations that may persist beyond 2024. From $1.5 trillion to $4.7 trillion in cumulative revenue could be lost between 2020 and 2024.”

The warning signals are clear as 77% of the banks did not return their capital in 2020. The average return on equity does not cover the cost of equity in 83% of countries, up from 71% last year.

With the pandemic turning the global scenario disappointing, Finance Minister Nirmala Sitharaman in her Budget had little option but to look to the private sector to bolster the confidence in the banking industry despite the government owning around 80% of banking assets. In this context, it is worth revisiting the status of Indian banking before nationalisation, post liberalisation and now, the call for privatisation.

Institutional reach widened through Banking Correspondents, opening of small finance banks and small payment banks in the private sector, though they are yet to fill the gap. Fintech and payment applications have accentuated cyber risks that the governments are trying to grapple with.

Pre-nationalisation

Pre-nationalisation, Indian banking had two phases: The first phase brought synergies in size with the merger of Bank of Bengal, Bank of Bombay and Bank of Madras into Imperial Bank of India (IBI). The IBI held the treasury of the British Empire in India. The ownership was transferred through the SBI Act, 1955, with the Reserve Bank of India and the government of India jointly owning it with the private shareholders of IBI continuing as legatees. 14 banks were nationalised in 1969 during Indira Gandhi’s regime, merging the social banking concept ushered in by Morarji Desai.

Several private banks were in the hands of the businessmen, known as multanis, and industrialists. To cite a few — Central Bank of India, Bank of India, Andhra Bank, Syndicate Bank, Vijaya Bank, Lakshmi Vilas Bank and Federal Bank. There were princely banks like the State Banks of Hyderabad, Mysore, Indore, Bikaner and Jaipur, Bhavnagar, Travancore. Later, the State Bank of Bikaner and the State Bank of Jaipur merged and formed the State Bank of Bikaner and Jaipur. In the second phase (1980), six more banks were nationalised. All the princely banks were made Associate Banks to the SBI.

The ICICI, IFCI and IDBI were the three institutions dedicated to financing infrastructure development. State Finance Corporations were set up under State statutes to finance industrial development in the State with term lending/investment credit while the matching short-term credit was to be provided by commercial banks. These were basically project finance institutions.

First Merger

In 1993, the government merged The New Bank of India and The Punjab National Bank and this was the first merger between nationalised banks.

The spirit behind nationalisation of banks is worthy of recall — both in the context of economic growth and financial inclusion as also the size. The Narasimham Committee (1991) put it thus: “Nationalisation was recognition of the potential of the banking system to promote broader economic objectives such as growth, better regional balance of economic activity and the diffusion of economic power. It was designed to make the system to reach out to the small man and the rural and semi-urban areas and to extend credit to coverage to sectors till then neglected by the banking system and positive affirmative action in favour of agriculture and small industry in place of what was regarded as somewhat oligopolistic situation where the system served mainly the urban and industrial sectors and where the grant of credit was seen to be an act of patronage and receiving it an aspect of privilege.”

The Lead Bank Scheme triggered branch expansion into rural and semi-urban areas. Credit to social sectors and the poor was through the designated priority sectors and weaker sections of the population. District administration was involved in the process of planning and implementation. For judging expansion, per branch population was the basic parameter followed by Deposit-Credit ratio.

Post nationalisation, growth of banking, geographically, made rapid strides. Mobilisation of deposits, extension of credit to the needy and credit-deposit ratio in rural areas improved.

Post-1991 Reforms

It was during the post-1991 reforms that cleaning up of banks and introduction of income recognition and asset classification norms, supervision through CAMELS (capital adequacy, asset quality, management, earnings and liquidity), entry of new private sector banks and introduction of universal banking public sector banks — which occupy 73% of banking space in India — moved away from social banking to commercial banking in its true sense with an eye on profits as the final goal for sustainability.

Banks that were blaming directed lending for the pile-up of non-performing assets (NPAs) at the beginning of the 1990s ended up accumulating NPAs to the order of Rs 8.29 lakh crore by June 2017 — mostly due to hasty lending to corporates. Indian Bank, Syndicate Bank, PNB had their heads suspect.

Private banks ICICI Bank and HDFC Bank were able to steal the march over the PSU banks through their retail lending and housing and real estate business along with vigorous branch expansion. Then, there were other older private sector banks like Karur Vysya, Vysya Bank (later became IngVysya Bank Ltd), South India Bank, Kotak Mahindra, Federal Bank which posed stiff competition to the PSU banks.

Meanwhile, institutional architecture for rural lending was strengthened following the Sivaraman Committee’s recommendations with the statutory formation of the National Bank for Agricultural for Rural Development (Nabard) in 1981. Nabard was to take care of the entire refinance of the commercial banks’ lending to agriculture and rural development.

Since the beginning of 1990, the banking system underwent dramatic changes in functional aspects such as customer service, resource mobilisation, credit management, credit liability, investments and HR development, with the reforms progress gathering momentum. But it was also the time when, along with the progress of reforms, banks started losing the trust of their clientele.

Creeping in Problems

The Narasimham Committee-I report (1991) made a strategic judgment that the problems of Indian banking were not fundamentally attributable to public ownership, but rather to the managerial and policy environment within which the banks operated. It drew attention to the high cost, poor service, poor loan recovery, low profitability and weak capital position of virtually all public-owned banks. The main explanations provided for this state of affairs was excessive centralisation and political interference, which undermined institutional autonomy, pride, and accountability in banks.

Following the committee’s recommendations, interest recognition and asset classification (IRAC) norms were introduced. Banks also went in for computerisation to render efficient service. As most banks were under severe losses, social banking goals took a back seat. Demand, Collection, Balance (DCB) registers introduced to monitor the recoveries in the farming sector and rural finance sector gave way to computerised monitoring of NPAs.

The Narasimham Committee-II (1998) recommended reduction of government holding in PSU banks to 33%, mergers and acquisitions of banks to nurture healthy units, FDIs, recruitment of skilled personnel, redefining vigilance of banking, strengthening information, control and asset liability management systems and treasury management, speeding collection of repayments, elimination interest subsidy for priority sector and increasing Capital to Risk weighted Assets Ratio, among others.

Their areas of challenges at that point were restructuring and reorganising banks’ setup towards thinner and leaner administrative offices, closing and/or merging of unviable metropolitan branches, developing new products and services that would meet the emerging customer needs. These reforms took a toll on the weak and inefficient ones. Creation and nurturing of the diversified, efficient functioning system with appropriate incentive framework was required.

Shaktikanta Das, RBI Governor, speaking at Ahmedabad University in 2019, recalled the status of banking pre-nationalisation:

“Five cities in the country, viz, Ahmedabad, Mumbai, Delhi, Kolkata and Chennai accounted for around 44% of the bank deposits and 60% of the outstanding bank credit in 1969. This led to the widespread political perception that, left to themselves, the private sector banks were not sufficiently aware of their larger responsibilities towards society.” Quoting RBI’s History of Banking Vol III, he said, “nationalisation of banks was thought of as a solution for greater penetration of banking that excluded 617 towns out of 2,700 in the country. And, even worse, out of about 6,00,000 villages, hardly 5,000 had banks. The spread, too, was uneven……”

Driving Inclusion

In the 50 years after nationalisation, banks strived to increase their reach through technology, expansion of branches, competition and BC. But banking still continues to be metro-centric. The figures of 2018 speak for themselves.

Metro centres (53) have a share of less than 20% in branches but with 51% of deposits, lent 64% of total advances as at the end of December 2018. Urban areas seem to be the worst affected: with a percent less in branches, they had a share of just 21.5% deposits and a mere 15% of the total advances.

While the credit-deposit ratio of metros is 96.5%, it is just 54.8% in urban areas. While the reach in rural and semi-urban areas is 62%, their share in deposits is 10.5% and 16% respectively while in advances, the corresponding share is 8.5% and 12.4%.

Technology-driven banking came in through the inclusion of electronic fund transfer, Any Place Deposit, Any Time Money, cyberbanking and e-commerce at numerous public bank branches. With the same objective, the RBI set up an apex institute — Institute for Development and Research in Banking Technology — and the State Bank of India its own institute in information technology.

The Narasimham Committee-II recommended winding up of the Department of Financial Services and merging with the Finance Ministry and also winding up of weak banks instead of merging them with strong banks. Both these recommendations are yet to merit the attention of the ministry.

Renewed Rural Focus

Noticing that rural infrastructure required specific funding and efficient monitoring of investments, Manmohan Singh as Finance Minister introduced Rural Infrastructure Development Fund (RIDF) carving out of the unused priority sector targets of commercial banks.

Since banks were new to this type of transition and the ageing human resources could not cope with the required efficiencies in handling the computerised systems, Know Your Customer norms were made mandatory. This made the identification of the customer easy and new accountability norms crept in. Finding some deficiencies in implementation, the RBI introduced KYC audits.

Since we did not resort to full convertibility of foreign currency assets, the collapse of Southeast Asia (1997-98) followed by Japan could not affect India. External rating of assets was made mandatory. CRISIL, ICRA, SMERA, Fitch, S&P, Moody’s entered the fray.

CIBIL was set up to provide online rating of individuals to the banks. All these, however, did not prove a boon to the lenders. It was the best-rated institutions that defaulted most and frauds involving billions of rupees with the perpetrators seeking international asylum like Vijay Mallya, Nirav Modi, Choksi shook the confidence in the lending system.

Deviating From Core Strength

Fresh recruitments into PSU banks started 15 years after liberalisation and the selection process was skewed in favour of engineering and software students. Knowledge of systems took precedence over the domain knowledge of banking. With little knowledge of infrastructure financing, real estate and housing, banks took to lending for them depending upon third-party assessments. Credit risk management that was once their strength has become a severe casualty. Armchair (‘lazy’, to quote YV Reddy) banking became the order of the day.

After Raghuram Rajan assumed charge as RBI Governor in 2014, he introduced Asset Quality Review and prompt corrective action with a view to purging banks loaded with toxic assets and NPAs.

Lessons from 2008

Lessons from 2008

The decadal data between 2000 and 2020 indicates growth in advances in both private and public sector banks and their NPAs too. However, to expect banks to lend without NPAs will be amounting to calling on banks to give up risk appetite. Also, creating mega banks would not extinguish either their toxic assets or reduce their losses. The government ignored the experience of the 2008 recession that warned ‘too big to fail’ banks would demand more resources from the exchequer than earlier.

The 2008 recession also led to demand for nationalisation in the UK, Australia, and the US to save the interests of the depositors and bond-holders. The very purpose of nationalisation– namely, serving the unbanked and under-banked — is yet to reach its frontier. Financial inclusion cannot afford the luxury of complete privatisation. In fact, coexistence of private and public sector banks would lead to a healthy competition if governance issues in PSU banks are adequately addressed.

It is wise to turn the pages of reforms suggested by the Narasimham Committee-II and reiterated at Gyan Sangam-1 (Retreat for Banks and Financial Institutions), that the government would do well to provide full autonomy to the PSU banks, and not interfere in transfers and postings, and issue of loans. Behest lending should stop with setting goals by the RBI. Owner cannot be regulator. It can at best be a supervisor to ensure their healthy functioning.

(The author is a former senior banker and risk management specialist)

Now you can get handpicked stories from Telangana Today on Telegram everyday. Click the link to subscribe.

Click to follow Telangana Today Facebook page and Twitter .

Related News

-

PM Modi chairs high-level meeting to review West Asia crisis impact on India’s energy security

-

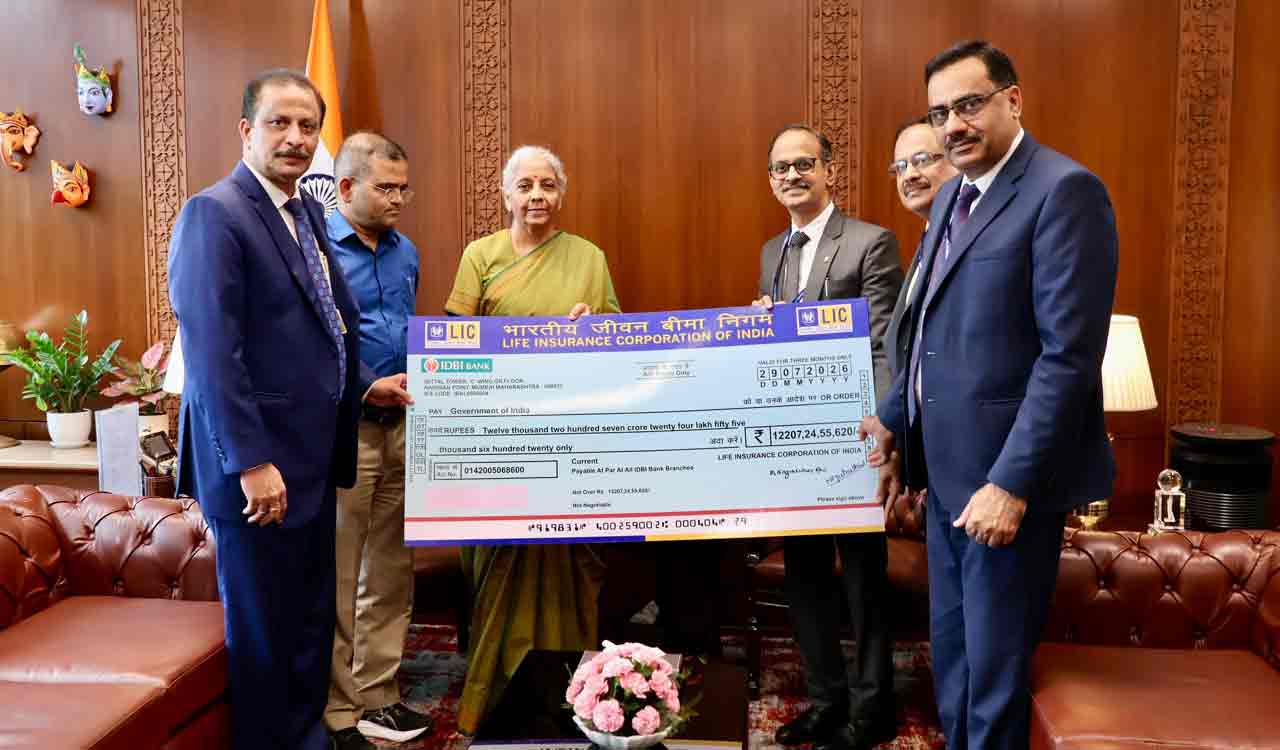

Finance Minister receives Rs 12,207 crore LIC dividend for FY 2025-26

-

Nirmala Sitharaman asks Income Tax officials to serve citizens better

-

She is a fool: Sanjay Raut attacks Nirmala Sitharaman over student paper leak comments