Banks need a new playbook

By B Sambamurthy Real GDP hit a decadal high of 8.2% during 2016-17. Since then, it has been on a downward slide and declined to about 4% during 2019-20. Covid-19 inflicted significant damage to economic growth and growth hurtled to a negative 6.5% in FY 2021. Keeping the impact of Covid-19 aside, the deceleration of […]

By B Sambamurthy

Real GDP hit a decadal high of 8.2% during 2016-17. Since then, it has been on a downward slide and declined to about 4% during 2019-20. Covid-19 inflicted significant damage to economic growth and growth hurtled to a negative 6.5% in FY 2021.

Keeping the impact of Covid-19 aside, the deceleration of economic growth has been placed nearly at the doorsteps of low bank credit growth during the last few years. The government and the Reserve Bank of India (RBI) have been exhorting banks to step up lending to boost economic growth and legitimately so.

Decelerating Credit Growth & Economic Growth

Bank credit growth hit a decadal high of 14% during 2012-13 and has been slowing down since then, reaching a low of 5.5% in 2020-21 triggering alarm bells in government corridors. There is both coincidence and correlation between credit growth and economic growth.

The government and the RBI have unleashed a series of measures, (still continuing) to prop up credit growth and thus economic growth. These measures include massive dollops of liquidity, liberal refinance lines, credit guarantee (up to 20%) for MSMEs and recapitalisation of PSU banks. Bank credit grew by about 8% during 2021-22.

A brief review of bank credit growth during 2021-22 reveals hits and misses

Personal Loans: Rs 35 lakh crore

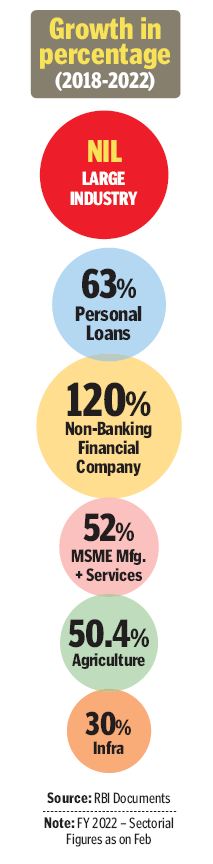

The personal loans segment emerges as a big winner, continuing its faster growth over the last decade. With an outstanding level of Rs 35.2 lakh crore (see table), it leaves behind credit to large industry (Rs 25.70 lakh crore) by miles. It grew by over 12.5% against large industry credit growth of 0.5%. It takes away over 43% of incremental credit growth and together with NBFC, it sucks away 58%. This no doubt fulfils aspirations of larger sections of people to own automobile, house, TV, fridge and other consumer durables.

This growth has also pushed up consumption-led growth. But it is a moot point whether household debt-fuelled consumption is sustainable in the long run. Whether personal loans are a substitute for employment and avenues for earning living wages is another debatable issue.

It is a moot point whether household debt-fuelled consumption is sustainable in the long run; whether personal loans are substitute for employment and avenues for earning living wages is also debatable.

Risk-adjusted returns are higher for lenders as compared with other sectors. It looks as though it is a win-win-win for personal loan borrowers, consumption-led economy and lenders. But this enthusiasm needs to be discounted if you go by the experience of other countries.

MSME: Manufacturing and Services: Rs 17.1 lakh crore

This segment has also grown by 13.5% on the back of nearly 20% growth in the previous year. This comes further on the back of Mudra loans a couple of years ago. The government’s ECLGS (Emergency Credit Line Guarantee Scheme) guaranteeing 20% of the loan has given a fillip to the credit growth. This has given a lifeline to micro and small enterprises, which account for over 80% of the credit. This segment is highly vulnerable to vagaries of economic cycles and technology disruptions and has little buffers.

These measures notwithstanding, mortality remains high. Very few graduate to medium sector and still fewer from medium to large industry. As guarantee is limited to 20%, one would assume that lenders have not compromised due diligence.

Agriculture

The agriculture sector credit grew 9.6%. There is a need and opportunity for massive investments in logistics to ensure better incomes for farmers, particularly for small/marginal farmers. Lenders need to focus on faster adoption of agri-tech to improve productivity and efficiency, and reduce risks across the value chain.

Infrastructure: Rs 11.90 lakh crore

Lenders to this sector were badly bruised over the last decade. Loss given default in some of the cases is very high at over 90%. But this sector is vital for achieving higher economic growth as it has the highest growth multiplier of all the sectors. Bank lending has resumed and recorded a growth rate of 11.2%. The problems are largely not lack of credit flow but other administrative and policy bottlenecks.

The Central government recently launched Gati Shakti Mission to reduce delays, cost and time overruns. It has already identified 130 critical projects with significant gaps. The newly launched Development Finance Institution may do the heavy lifting. Small and medium category lenders may like to know why even the big lenders headed by scholars could not identify and mitigate risks of lending to this sector and they pivoted to the retail /personal sector effectively. Developments in this sector have huge implications for achieving the $5 trillion economy.

Large Industry: Stagnant at Rs 25 lakh crore: Scissors Problem

Credit flow to large industry has been lacklustre over the last few years and this trend continued this year as well. It grew by a measly 0.8%. As per the recent Economic Survey, industry’s share in gross value added (GVA) growth fell from 9.6% in 2016 to a negative of 1.2% during 2021. Similarly, manufacturing growth plummeted from 13.1% to minus 2.4%.

Given the fact that big-ticket loans accounted for as high as 70% NPAs, it is only natural that risk appetite is diminished, which in turn constrains supply

Large private sector lenders having suffered huge losses in the earlier decade have pivoted to the retail sector. Massive write-offs of previous years have tapered off during this year. Some of the well-rated corporates have been accessing debt markets directly and banks invest in some of these issues. Some of the corporates have also deleveraged taking advantage of booming capital markets. Even reckoning these factors, there is not much eagerness to lend to this sector.

This sector faces both demand and supply problems and many call this the Scissors problem. Firstly, the demand for funds for fresh investments is subdued due to the availability of installed capacity. Capacity utilisation hovers around 70%. Secondly, the fact that some of the well-rated corporates can borrow at repo or subpar Repo rates (4%) indicates weak demand for new investment loans. This also reflects intense competition among banks for big-ticket loans and even to lend at a negative net interest margin (NIM).

Given the fact that big-ticket loans accounted for as high as 70% NPAs and some of the banks incurred NPAs as high as over 15-20%, it is only natural that risk appetite is diminished, which in turn constrains supply. There is no gainsaying the importance of bank credit flow to large industry, particularly for new investments. The recently announced production linked incentive (PLI) scheme may perk up demand for new investment credit.

Real Growth Engines & Fuel

From a broader perspective, the economy is driven by three engines: viz Exports, Investment and Consumption. Bank credit, it may be said, provides fuel to these engines of growth at an affordable cost with due care. The altitude and trajectory of growth depend much on the efficiency of the pilots flying these engines. If they fly low and slow, much of the fuel (bank credit) gets wasted and even turns toxic (NPA).

Government, entrepreneurs and consumers pilot these engines. These growth engines have been sputtering during the last few years for various reasons. Nonetheless, the link between credit and economic growth must not be underestimated in a bank-dominated economy like ours. Bank credit is both a consequence and a cause of economic growth. Fiscal and monetary policies keep them going in a virtuous cycle.

The altitude and trajectory of growth depend much on the efficiency of the pilots flying these engines. If they fly low and slow, much of the fuel (bank credit) gets wasted and even turns toxic (NPA)

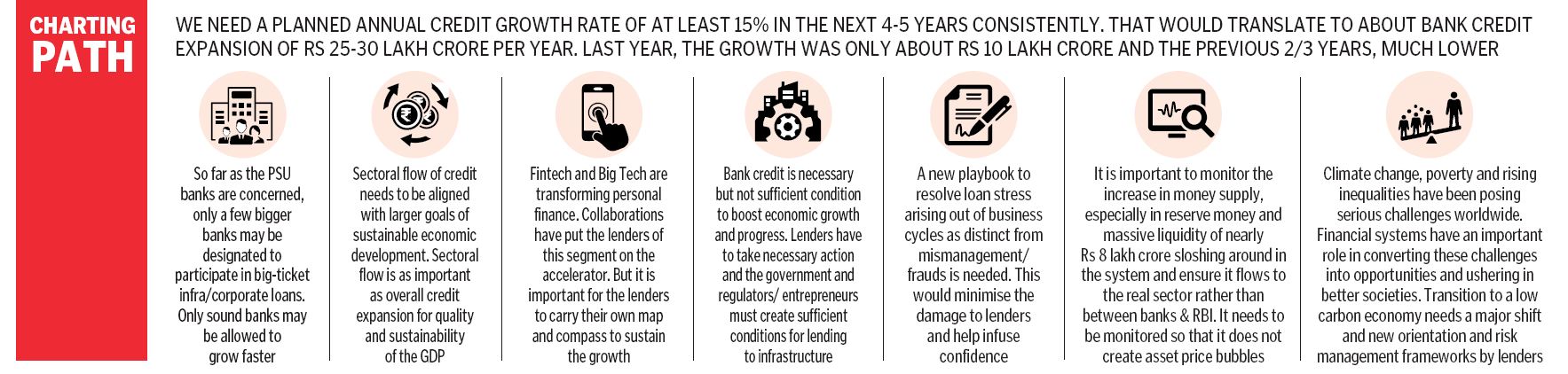

An IMF working paper (11/278) by DenizIgan and others argues that credit booms are followed by credit crises with a lag and at times threaten financial stability. The research covers 90 credit booms in over 90 countries, including India. What is a credit boom? Where to strike a balance? Macro-level credit boom is a call for regulators and micro-level boom is a call for boards and shareholders? The RBI in its latest report puts this optimal credit growth at 13%.

Having substantially cleaned the balance sheets of banks, it is vital a new ecosystem is created to facilitate higher credit growth and at the same keep gross NPAs (non-performing assets) at a low level of say 2%. Regulators, government, entrepreneurs, market infrastructure players have their tasks cut out.

Is the new playbook ready?

(The author is a former PSU Bank Chairman)

Now you can get handpicked stories from Telangana Today on Telegram everyday. Click the link to subscribe.

Click to follow Telangana Today Facebook page and Twitter .

Related News

-

Net FDI drops to USD 6.95 billion in FY26 amid higher repatriation, ODI outflows: Govt

-

India-UK FTA to Boost Trade to $115 Billion by 2030, Create Up to 10 Lakh Jobs: Assocham

-

Rupee falls 20 paise to Rs.96.73 against US dollar as crude prices surge on West Asia conflict

-

Rupee slips 4 paise to 96.57 against US dollar amid rising crude oil prices