Opinion: Regulating MFI industry

By Seela Subba Rao Microfinance institutions (MFIs) have evolved into a vibrant industry exhibiting a variety of business models. In India, they exist as NGOs (registered as societies or trusts), Section 25 companies, NBFC-MFIs and other NBFCs. Commercial banks, regional rural banks, cooperative banks and other large lenders have played an important role in financing […]

By Seela Subba Rao

Microfinance institutions (MFIs) have evolved into a vibrant industry exhibiting a variety of business models. In India, they exist as NGOs (registered as societies or trusts), Section 25 companies, NBFC-MFIs and other NBFCs. Commercial banks, regional rural banks, cooperative banks and other large lenders have played an important role in financing MFIs. Banks have also leveraged the SHGs channel to provide direct credit to borrowers of groups.

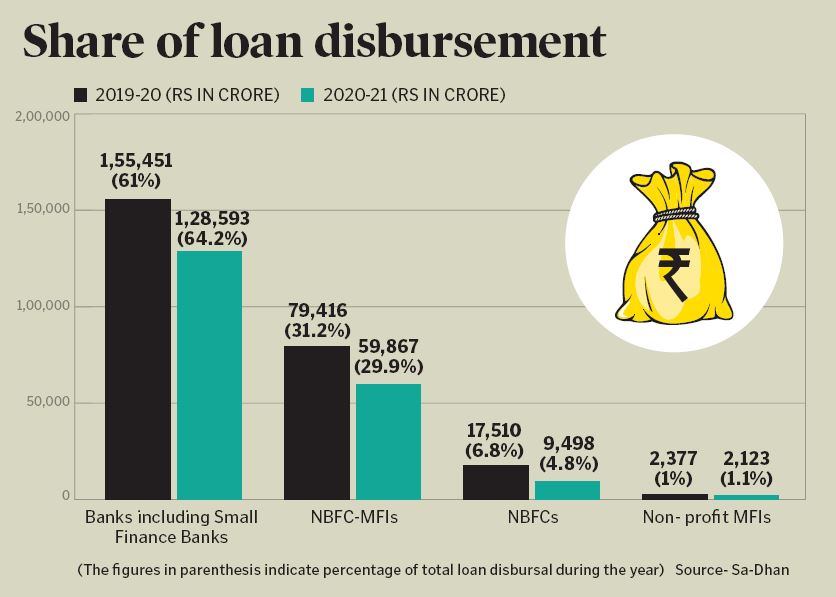

As per a Sa-Dhan report, the microfinance industry disbursed Rs 2,54,754 crore and Rs 2,00,081 crore during 2019-20 and 2020-21 respectively. Though banks and NBFC-MFIs, which cover a major part of loan disbursal by the microfinance channel, are regulated by the Reserve Bank of India (RBI), other NBFCs such as societies, trusts and Section 25 companies fall outside the purview of the RBI. Regulation serves to ensure the financial soundness of an MFI and reinforces public trust in these institutions.

MFI Bill

The MFI (Development and Regulation) Bill, 2012, was a major step taken by the Central government in the microfinance sector. It was introduced in the Lok Sabha on 22 May 2012 and referred to the Standing Committee on Finance on 28 May 2012. The committee under the chairmanship of Yashwant Sinha submitted its report on 13 February 2014.

The Bill seeks to provide a statutory framework to regulate and develop the microfinance industry and also provides for setting up a Microfinance Development Fund managed by the RBI. The proceeds from the fund can be used for disbursal of loans, refinance or investment in MFIs. It has a provision to create a grievance redressal system and provides safeguards against excessive interest rates. It allows RBI to set upper limits on lending rates and margins and also allows MFIs to take up pension and insurance services.

The Bill proposes the setting up of a microfinance development council with members from Central government ministries, RBI, Sidbi, Nabard, NHB etc. For greater involvement of the States, the Bill proposes the setting up of State Development councils with representatives from the State government. District Microfinance Committees will also be set up to closely monitor the MFIs.

Schools of Thought

One school of thought advocates that there is a need for a statutory body for the regulation and supervision of entities involved in the microfinance business. Self-regulation has never worked in microfinance as experience shows such as Kolar 2009 and AP 2010 crises. The role of self-regulatory organisations such as MFIN and Sa-Dhan is noteworthy but their functions are advisory and not statutory. The system of an ombudsman may also not be effective since most MFI borrowers are poor and illiterate. It is too much to expect that they will travel all the way to make a complaint with the ombudsman.

Some experts are of the view that MFIs should be under a specially created body called Microfinance Regulatory and Development Authority (MFRDA), like IRDAI and PFRDA, for grievance redressal.

Another school of thought is of opinion that the existing system may continue. The cost factor involved in regulating/supervising such a large number of entities across the country should be considered. MFIs affiliated with MFIN, and Sa-Dhan are following the fair code of conduct formulated by the latter. Setting up a separate regulator exclusively for other MFIs with a meagre loan portfolio appears not prudent.

Also, there is a multiplicity of legal forms of entities engaged in the microfinance sector. The authorities concerned with whom these institutions are registered have the prime responsibility to control, supervise and audit their books periodically. Hence, a separate regulator/supervisor is not warranted.

A separate legislation for the development and regulation of MFIs has not picked up momentum even though its need was deliberated by the Standing Committee on Finance during 2012-2014. The committee members opined that since the RBI performs onerous duties as the central bank of the country, it is not advisable to burden it further. However, the members were inclined to suggest the constitution of a unified and independent regulator for the sector as a whole.

It further mentioned that wider consultations with stakeholders and deeper studies on vital issues are needed to arrive at a consensus. Hence, the committee urged the government to reconsider the proposals contained in the Bill in all its ramifications and bring forth a fresh legislation before Parliament. So far, no progress has been made in this direction. It is felt that a centralised legislation would be inappropriate with regard to the microfinance movement which was meant to be essentially informal and decentralised.

Designing a System

Some MFIs have been accused of presenting opaque loan terms, charging exorbitant interest rates, mis-selling of micro-credit products, etc. Therefore, there is a need for a redressal mechanism to protect the MFI clients. The Consumer Protection Act, 1986, specifies a redressal mechanism under which quasi-judicial bodies have been set up to resolve disputes quickly. If micro-credit is covered under the Consumer Protection Act, various forums at State/district level can be extended to provide the requisite redressal.

Banks and NBFC-MFIs contributing a lion’s share of loan disbursal to the MFI industry are regulated by the RBI. Hence, setting up a separate regulator/supervisor for the MFI industry needs consultations with State governments and other stakeholders. Given the existing Indian financial regulatory structure, an MFI regulator would inevitably have overlaps with other financial regulators. Money lending regulations of respective States can deal with the adverse situation.

The expansion of MFIs is much needed to serve more people, especially in unbanked areas. Several improvements to the sector’s operating model must also be implemented, including digital interventions in the lending value chain. Further, the MFIs, known as the ‘last mile financier’, need to evolve a large range of financial products out of a pure credit services role.

(The author is former Assistant General Manager, Nabard)