Opinion: Whopping haircuts and IBC reforms

The scorecard in terms of recovery/resolution value of many of the big accounts is quite underwhelming

The Insolvency and Bankruptcy Board of India (IBBI), no wolf warrior, disrupted the resolution and recovery regime for good. Judicial pronouncements validating IBC only sharpened its teeth and claws for good. It left the dilatory regimes like DRT (Debt Recovery Tribunal), BIFR (Board for Industrial and Financial Reconstruction), SARFASEI, and ARC (Asset Reconstruction Company) miles behind.

The resolution process under the Insolvency and Bankruptcy Code (IBC) is now counted in terms of days and not years or decades as earlier. It sent signals and not just noise that errant borrowers would lose divine right to continue to own and manage the very companies that they pushed into insolvency. Ease of doing business is another gain. Credit culture too shows signs of improvement. It is huge progress.

Recoveries Meek, Measly: Peanuts?

But the scorecard in terms of recovery/resolution value of many of the big accounts is underwhelming if not dismal. There are several major cases, which have suffered whopping haircuts of over 70% and in some cases, even 95%. Apparently, flabbergasted at the measly settlement of 5% in a recent case, the National Company Law Tribunal (NCLT) while approving, dismissively characterised it as peanuts.

Reacting to these steep haircuts, Harsh Goenka in a recent statement, said “hard earned public money being stolen as companies’ promoters stash away money on the side”. Coming as it does from an eminent businessman, this may be ignored at lenders/government peril.

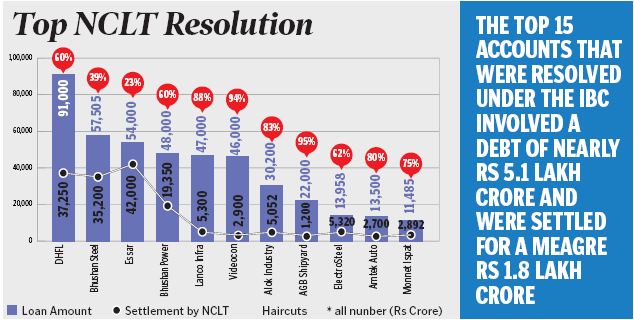

These huge haircuts leave a jarring note among the public, small borrowers and depositors. The top 15 accounts that were resolved under the IBC involved a debt of nearly Rs 5.1 lakh crore and were settled by the NCLT for a meagre Rs 1.8 lakh crore. Thus banks, financial and operational creditors lost a whopping Rs 3.3 lakh crore. The down payment is hardly 10-15% of the resolved value, often equivalent to cash sitting in the company and the rest of the settled money is payable only after several years through fresh IOUs. One is not sure whether these massive haircuts were envisaged by the committee that recommended the IBC legislation.

Facts, Truth and Valuations: Bugbear of IBC

Valuation by the IBBI-appointed valuers is the (safe) reference point for accepting the bid prices by prospective buyers. But in many cases, these valuations are many times much lower than the value of assets certified by defaulting company auditors nearer to the insolvency date. Valuation by the company’s auditor is higher, ranging from two times and in some cases 2/10 times.

In oft-quoted big recent case, the difference in valuation is almost 13 times. The IBBI-appointed valuers certify values under Fair Value method and auditors of companies also certify values as True and Fair with some caveats. It is accepted that valuation varies from scenario to scenario and context. But that does not explain such low valuation by IBBI valuers.

One does not know for certain whether bid prices are ‘dirty’ or valuations are ‘dirty’ or price discovery is not effective and efficient. The gulf between these valuations may vitiate the IBC process and should not leave scope for misuse. The IBBI needs to address this, including process and models.

Trace Funds Quickly

If the assets are gold plated, as is widely believed in many cases and funds siphoned off, it is imperative that these siphoned off funds are recovered early and restored to the lenders. In a recent case of ransom payment for a cyber attack on a US gas supply company, the FBI traced and blocked the money, which was routed through over 20 entities globally to a digital wallet in a matter of few days.

Stress Not Asymptomatic

A non-performing asset (NPA) is an interplay of business stress and financial stress, and these are not asymptomatic, at least to the directors and auditors. Badly run companies have been hiding losses (NPA) behind new borrowings and carrying on business year after year and only piling up losses and pushing the company into inevitable insolvency. The IBC terms this as wrongful trading (Sec 66), which the directors are obligated to know. This law slaps liability on directors and others if they do not take action to halt such wrongful trading and minimise losses to the creditors.

The enforcement of these provisions needs to improve so that huge haircuts may be mitigated. Fail early and fail small is a useful business strategy and helps cut losses, both for businesses and lenders.

Capacity Building: IBBI 2.0

Resolution Professionals, Valuers, Committee of Creditors, NCLT, IBBI and other stakeholders are new to the game. Many of them have no adequate experience in handling valuation and resolution of enterprises/conglomerates involving tens of thousands of crores, and that too a complex web of corporate networks.

It is not known how many of them earlier handled cases involving even hundreds of crores, leave alone tens of thousands of crores. The size and complexity of these accounts would be overwhelming for many of these functionaries. As such, it is not difficult to game the system. This needs urgent and massive capacity building across the entire ecosystem.

Separating victims from villains is another exercise. Goenka’s lament is a wake-up call to review IBC afresh and plug the loopholes without delay. Besides mitigating losses, this would put a stop to de-motivating genuine and disciplined risk-takers and entrepreneurs.

Way Forward

• Enforce wrongful trading rules in time and inculcate a culture of Fail Small and Fail Early. This helps in early recognition of irreversible business stress and NPAs and thus minimises losses to all stakeholders. The important lesson is ‘DELAY is DECAY’.

• Revisit valuation process and valuation models to get realisable value. IBBI needs to orchestrate dialogue between valuers and borrowers’ auditors in the presence of COC to get a true if not factual valuation. Double/Triple blind valuations can mitigate subjectivity.

• Haircuts, in many cases, hover around $1-6 billion and stressed asset market is over $150 billion. This is global scale. It is imperative that all the functionaries have very high degree of skill and capabilities. Capacity building across the entire ecosystem of resolution framework brooks no delay. Create a global market for price discovery and participation.

• Given the huge stakes, one may not be faulted to assume that various IBC functionaries are vulnerable to sabre-rattling. IBBI needs to build some guard rails, checks and balances to ensure a high degree of integrity and skills so that commercial decisions are of high quality. Auction models may be changed for better price discovery and ensuring confidentiality of valuations.

• Case studies offer useful lessons to all stakeholders — to lenders on better underwriting and monitoring practices, to regulators on supervisory practices and forbearance policies and to the government in the case of PSU banks on advisories for lending.

These measures, if well implemented, can bring down the haircuts by at least 25%, which may translate to about Rs 1 lakh crore.

Heard long ago we have only sick industries but not sick promoters. Does it hold true in the IBC regime as well? Does this process produce IBC billionaires? NPAs are inevitable (maybe under 2%), but 70%+ haircuts are not.

(The author is former Director, Institute for Development and Research in Banking Technology)\

Now you can get handpicked stories from Telangana Today on Telegram everyday. Click the link to subscribe.

Click to follow Telangana Today Facebook page and Twitter .