Hyderabad hub for Grade-A malls

With more than 3.9 million sqft Grade A space leased during January–June, Hyderabad had more than 52 per cent of the total grade A space in the country.

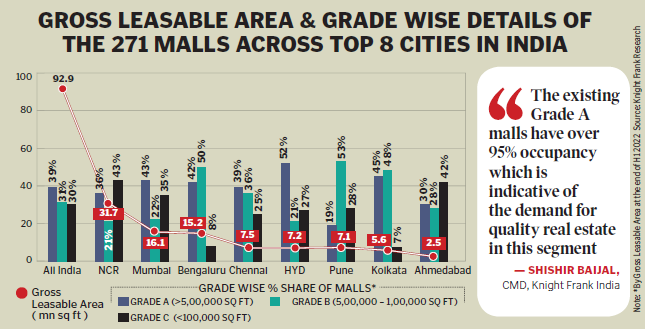

Hyderabad: Hyderabad is a preferred destination for malls. With more than 3.9 million sqft Grade A space leased during January–June, Hyderabad had more than 52 per cent of the total grade A space in the country.

While 93 million sqft was leased during January to June this year, about 7.2 million sqft happened in Hyderabad. The share of Grade B and C malls stood at 21 per cent (1.57 million sqft) and 27 per cent (2.02 million sqft) respectively.

Also Read

At the country level, Grade A mall space was 36 million sqft or about 39 per cent of the total stock in the first half of the year.

Grade A mall is characterised by high occupancy, strong tenant mix, good positioning and active mall management. Grade B mall stock has decent occupancy and tenant mix. Grade C malls have high vacancy rates, poor tenant mix, and relatively poor mall management impacted the contribution by Grade C malls.

“Smaller sized and lower grade developments are giving way to Grade A malls. The existing Grade A malls have over 95 per cent occupancy which is indicative of the demand for quality real estate in this segment,” says Shishir Baijal, Chairman and Managing Director at Knight Frank India.

In FY 2023, the potential consumption in shopping malls across India is estimated to reach $11 billion. It is forecast to grow at a CAGR of 29% to reach $39 billion in 2027-28.

Real estate and investment management player JLL too said Hyderabad will be one of the key contributors to the malls’ segment along with Delhi, Mumbai, Pune, Bengaluru, Kolkata and Chennai.

The retail sector in the country was under duress for a long time due to the pandemic. However, since March 2022, there has been a swift recovery owing to the favorable demographics, rapid urbanisation, and rising consumption, says Rahul Arora, Head, Retail Business, India, JLL.

“Investors are looking for quality Grade A assets by established developers and having a marginal vacancy. With the retail market rebounding, the vacancy in superior Grade A assets has been declining constantly,” he adds.

Superior-grade malls are preferred by both consumers and retailers. More than 70 shopping malls with a total retail space of 31.02 million sft are expected to become operational by 2025 across the top seven cities of India. Delhi NCR and Chennai will contribute 48 per cent share. Bengaluru and Hyderabad also have a combined share of 30 per cent of total supply till 2025. Leasing demand in malls is expected to expand and surpass pre-pandemic levels by 2023.