Monetisation of National Assets

Though an important policy direction, National Monetisation Pipeline is fraught with risks, and requires careful planning and implementation

By Prof Sanket Mohapatra, Prof Viswanath Pingali

With the recent sale of Air India by the Government of India (GoI), the National Monetisation Pipeline (NMP) is back in focus among the public. While Air India is an outright sale, NMP is more about the long-run lease of national assets. Since the intent of both moves is to raise much-needed capital for the government, the sale did bring NMP into a sharp focus in recent times.

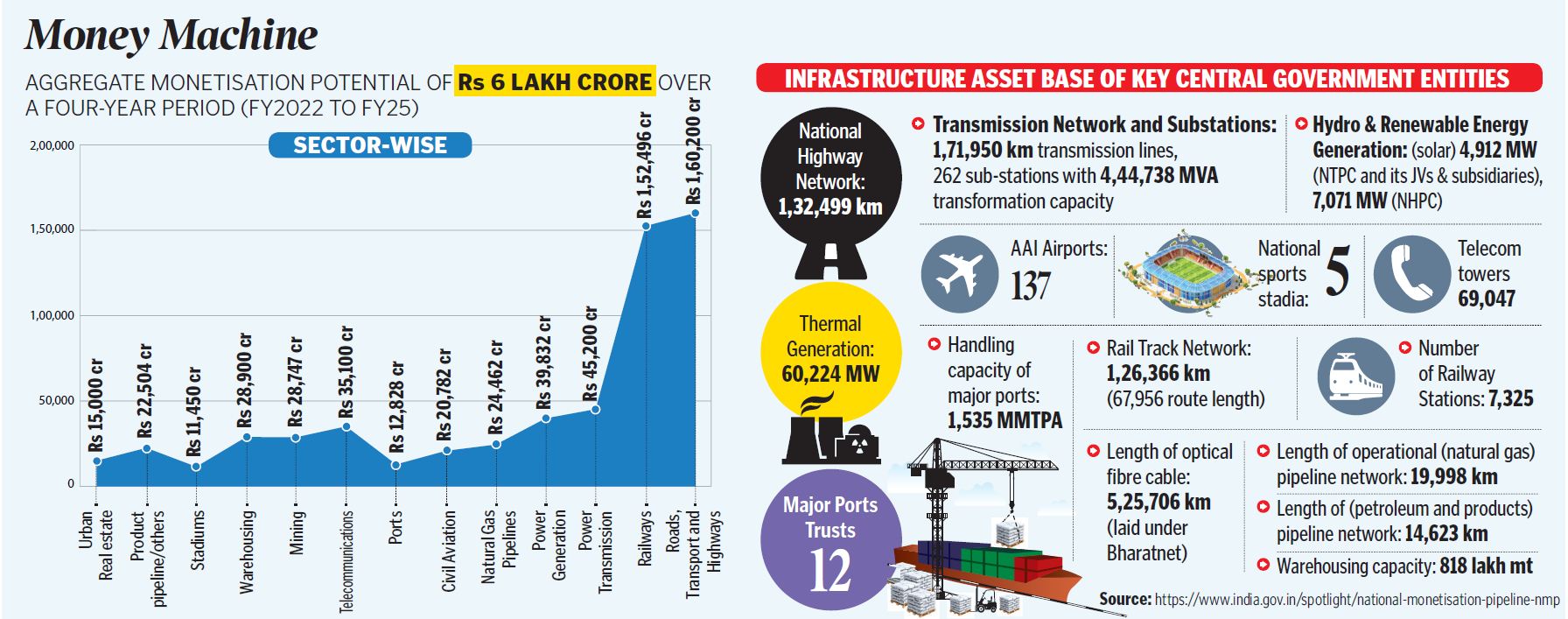

Through NMP, the GoI aims at monetising sovereign assets in roads, railways, aviation, power generation and transmission, telecom, mining, etc, and raise around Rs 6 lakh crore over the next four years. While it is an important policy direction, there are several risks, which need to be carefully analysed.

Some Advantages

Obviously, NMP has certain advantages. For starters, these additional revenues free up fiscal space for productivity enhancing expenditure on some key activities aimed at a sustained GDP growth. Development economists have long realised that the development of human capital is key towards sustained growth, and investments in sectors like health, education and infrastructure go a long way in achieving that goal.

Moreover, these investments tend to have a multiplier effect, especially because improvement in health/education has larger social implications than the group that receives these services. For example, the ongoing pandemic has clearly shown the importance of investments in healthcare. However, in order to take advantage of the multiplier effect, massive outlays by the government are required; NMP could be the source of such funds.

Private management of national assets would bring about efficiencies and improvements in service quality, as witnessed in significant enhancement in service quality of Indian airports since the late 2000s, bringing them closer to international standards. Such quality improvements can lead to greater willingness to paybythe end-users. If these quality enhancements happen in a sustained manner, maintenance of the nation’s transport infrastructure by the private players would reduce transportation and logistics costs for firms, bringing goods to both domestic and export markets faster and increasing India’s competitiveness. More reliable energy supplies by the private lease-holders and fewer outages would enhance the productivity of India’s corporate sector.

NMP also provides a steady revenue stream to the government for several decades vis-à-vis lumpy one-time sale of a state-owned asset or the alternative of a continuous drain on the public exchequer of keeping alive zombie public sector enterprises. That can help in better planning of the government’s expenditure in the future years. Even using the revenues to reduce the fiscal deficit can reduce government borrowing through issuance of government securities (G-Secs) and reduce yields, lowering the “crowding out” effect of government spending on private investment.

Inherent Risks

- Lack of All-round Participation

As much as NMP involves significant advantages, there are some inherent risks. First is that there may be a lack of all-round participation, as some of the previous public-private partnerships (PPP) have shown. We think that monetisation of existing public assets through long-term leases mitigates the risks inherent in previous PPP projects that involved approvals, environmental clearances, acquisition of land etc, — all of which introduced substantial uncertainty in future cash flows.

Mitigation of such risks can encourage greater participation of both domestic and international investors and improved realisation. In the post-Covid-19 world, where balance sheets of several firms are severely battered, strong corporate governance rules, including limits on who can bid, will be needed to ensure that these national assets do not end up in the hands of a handful of rich individuals.

- Possibility of Renegotiation

A massive deterrent against NMP is the possibility of renegotiation by subsequent governments, especially if the mechanism of allocation is questioned. A recent renegotiation attempt by the Andhra Pradesh government of power purchase agreements comes to mind.

For this to happen, we necessarily need to have a strong dispute resolution mechanism. As much as renegotiation should be possible, strong assurance that buyers’ interests will also be protected, is required. Presence of such risks tends to lower the potential valuation of the assets, and, therefore, requires the presence of strong sectoral regulators so that the right price for the assets can be obtained.

- Winner’s Curse

Another important factor to consider is that, typically, when these national assets are auctioned off, we see that the winner has significantly overbid for these assets. Economists term this phenomenon as the winner’s curse, and it happens when the winner of the auction is more optimistic about the asset than the competitors, which, at times can be over-optimism. Moreover, these losses are realised over a period of time, and not immediately after the sale.

This frequently leads to ex-post bailouts by the governments. As recent examples of no bids for some of these assets prove, it seems that Corporate India is learning, and, therefore, is refusing to bid so that the winner’s curse is mitigated. In order to avoid such contingency, more transparency on the assets being monetised is non-negotiable.

- Cherry Picking and Market for Lemons?

The most attractive government assets with assured returns have been included in the asset monetisation pipeline. There is a risk that the government may be left with “lemons” (the least productive assets) which may cause a drain on resources and eventually need to be liquidated. An important question arises in this context: Is it possible that the revenues realised by the government from the attractive assets (upfront payments and the subsequent tax payments) outweigh the costs of being left with lemons alone?

- In Times of National Crisis

Finally, these assets have come to the rescue of the country, especially in times of emergency. For example, Air India has been primarily used for evacuating Indian citizens out of regions prone to war (for example, evacuations out of Kuwait during the Gulf war, Djibouti (Operation Rahat) during the recent Yemen crisis, etc). Air India also helped significantly in helping the Indian citizens come back to India during the Covid-19 crisis.

With Air India moving into private hands, would the airline still be interested? In several cases, there have been reports that private airlines could have come to the rescue of the government if given a chance. Therefore, is it true that the national assets are the only help during the national crisis?

All in all, while it is clear that monetisation of these assets is fraught with a lot of risks, and, therefore, requires careful planning, there are obvious advantages. With better corporate governance practices, strong dispute resolution contracts, clauses so that dominance by a few individual players can be avoided, etc, this could be an initiative that could help the government significantly.

Further, a case-by-case analysis is very much required to understand the merits and demerits significantly. In short, it will help governments focus more on governing, than managing these! However, caution is needed; after all, the devil is in the details!

(The authors are faculty members in the Economics area of Indian Institute of Management Ahmedabad. Views are personal)

Now you can get handpicked stories from Telangana Today on Telegram everyday. Click the link to subscribe.

Click to follow Telangana Today Facebook page and Twitter .